# South Africa's Project Khokha: Pioneering Wholesale CBDCs in Africa

Central Bank Digital Currencies (CBDCs) are reshaping the future of finance globally, and Africa is no exception. Among the continent's most ambitious and technically advanced initiatives is South Africa's Project Khokha, a pioneering effort in wholesale CBDCs led by the South African Reserve Bank (SARB). In this article, we explore the significance of Project Khokha, its technical innovations, and its implications for Africa’s digital economy and financial infrastructure.

Understanding Wholesale CBDCs and Project Khokha

Wholesale CBDCs are digital currencies issued by central banks, designed specifically for use by financial institutions in interbank payments and settlements, rather than for general retail use. These CBDCs aim to enhance efficiency, transparency, and security in the settlement of large-value transactions.

South Africa’s Project Khokha, initiated in 2018 by SARB in collaboration with local banks and technology partners, is among the first African-led efforts to explore wholesale CBDCs using blockchain technology. The project’s objective is to assess the viability of blockchain-based payment systems in a real-world environment and to develop a prototype that could potentially replace or complement existing interbank settlement systems.

The name “Khokha” means “to strike” or “to knock” in Zulu, reflecting the project’s goal to “strike” a new path in financial infrastructure.

Technical Architecture and Innovation

Project Khokha’s technical foundation is built on distributed ledger technology (DLT), specifically leveraging Quorum, a permissioned blockchain platform derived from Ethereum. This choice enables privacy, scalability, and the ability to process large volumes of transactions — critical features for wholesale financial markets.

Key Features:

- Atomic Settlement: The project demonstrates atomic settlement of transactions involving central bank money, enabling simultaneous transfer of securities and funds without settlement risk.

- Permissioned Network: Only authorized participants (commercial banks and the central bank) can join the network, ensuring confidentiality and regulatory compliance.

- Interoperability Testing: Project Khokha has explored interoperability with other payment systems and potential integration with South Africa’s Real-Time Gross Settlement (RTGS) system.

- Stress Testing and Scalability: The platform has been subjected to rigorous stress testing, successfully handling thousands of transactions per second, showcasing its suitability for high-value interbank settlements.

These technical achievements place South Africa at the forefront of blockchain innovation in Africa’s financial sector.

Impact on South Africa and the Broader African Financial Ecosystem

South Africa is Africa’s most sophisticated financial market, with a well-established banking infrastructure and regulatory framework. Project Khokha’s success is a clear signal that wholesale CBDCs can enhance the continent’s financial systems by:

- Reducing Settlement Times: By enabling near-instantaneous settlement of large-value transactions, wholesale CBDCs could reduce counterparty risk and improve liquidity management for banks.

- Lowering Transaction Costs: Blockchain-based settlement systems can streamline processes, reduce intermediaries, and lower operational costs.

- Enhancing Financial Stability: Improved transparency and real-time monitoring of transactions may allow regulators to better manage systemic risks.

- Facilitating Cross-Border Payments: While Project Khokha is primarily focused on domestic transactions, its underlying technology creates a foundation for future cross-border payment solutions, a critical need in Africa’s fragmented financial landscape.

For example, the African Continental Free Trade Area (AfCFTA) aims to boost intra-African trade, yet cross-border payments remain costly and slow. Wholesale CBDCs could help harmonize payment infrastructures across borders, fostering regional integration.

Lessons for Other African Countries

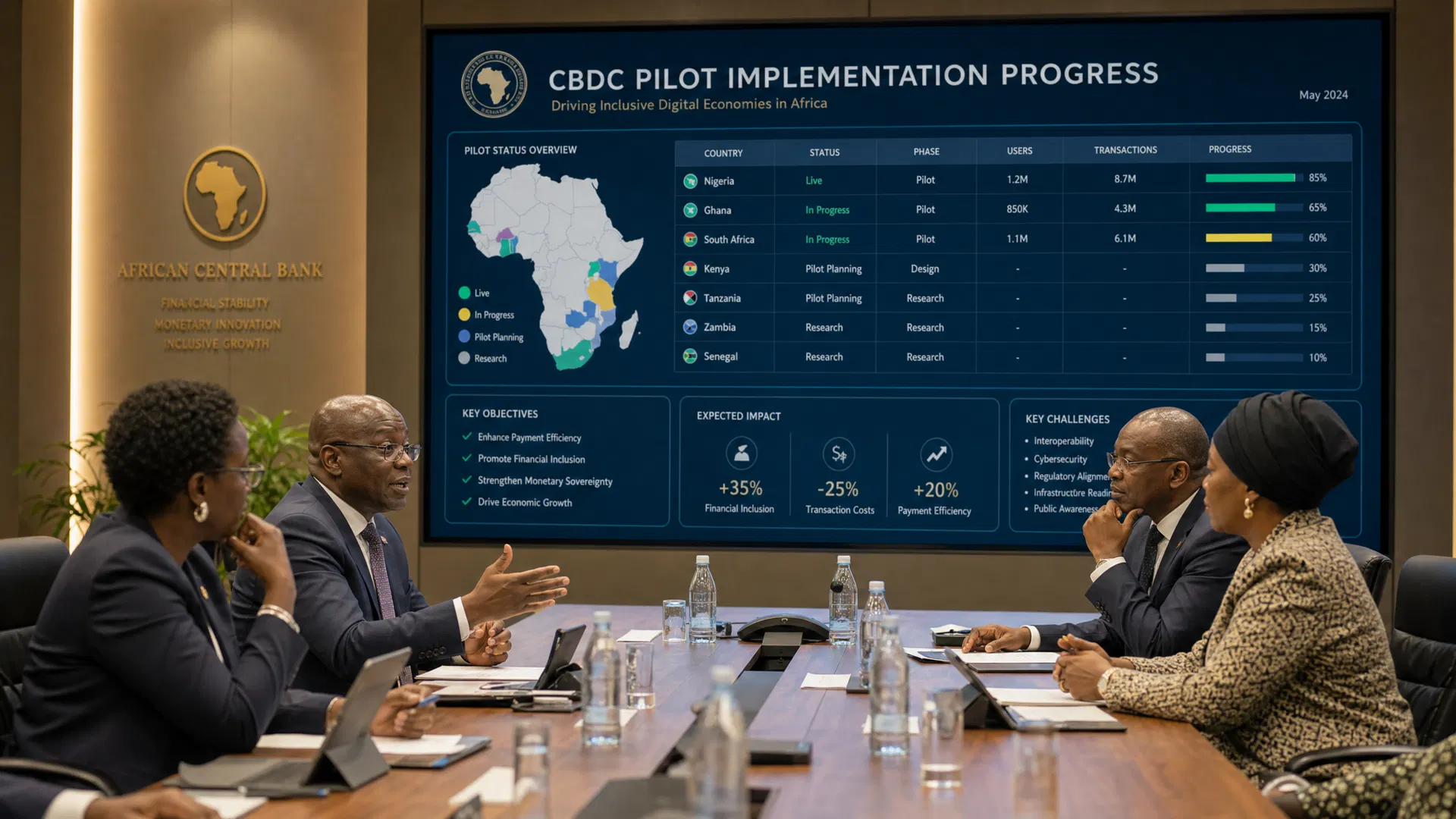

Several African central banks are observing Project Khokha closely as they consider their own CBDC initiatives. Nigeria’s eNaira and Ghana’s e-Cedi are retail CBDCs targeting individual consumers, but wholesale CBDCs have distinct use cases and benefits.

Countries like Kenya, Mauritius, and Rwanda, which have rapidly growing fintech sectors, could leverage wholesale CBDCs to modernize interbank settlements and reinforce financial market infrastructure.

Key takeaways for African policymakers include:

- Collaborative Approach: Project Khokha involved close collaboration between the central bank, commercial banks, and technology providers, setting a model for multi-stakeholder engagement.

- Regulatory Readiness: Project Khokha highlights the importance of adapting legal and regulatory frameworks to accommodate new digital payment systems.

- Technological Adaptation: African financial systems must invest in scalable, secure, and interoperable technologies to harness CBDC benefits.

- Capacity Building: Training and development are critical to ensure that regulators and financial institutions understand and can manage CBDC systems effectively.

Conclusion: Project Khokha as a Catalyst for Africa’s Digital Financial Future

Project Khokha represents a milestone in Africa’s journey toward a more efficient, transparent, and resilient financial ecosystem. By demonstrating the practical application of wholesale CBDCs in a complex banking environment, South Africa has positioned itself as a leader in blockchain-driven financial innovation on the continent.

As African economies continue to digitize, the lessons from Project Khokha will be invaluable in shaping policies, infrastructure, and partnerships that leverage CBDCs to drive economic growth, financial inclusion, and regional integration.

For institutional investors and policymakers, understanding the nuances of wholesale CBDCs like Project Khokha is essential for navigating Africa’s evolving digital finance landscape and capitalizing on emerging opportunities in the continent’s vibrant digital economy.