Retail vs. Wholesale CBDCs: African Central Bank Priorities

As the global financial landscape rapidly digitizes, Central Bank Digital Currencies (CBDCs) have moved from theoretical concepts to active pilot programs and live deployments. In Africa, central banks are increasingly exploring CBDCs to modernize payment systems, enhance financial inclusion, and improve cross-border trade. However, the approach to CBDC development varies significantly, primarily divided into two categories: retail and wholesale CBDCs. Understanding the distinction between these two models is crucial for institutional investors, policymakers, and stakeholders navigating Africa’s digital economy.

This article examines the differences between retail and wholesale CBDCs and analyzes the priorities of African central banks in their digital currency strategies.

---

Understanding Retail and Wholesale CBDCs

Before delving into regional priorities, it is essential to define the two primary types of CBDCs:

Retail CBDCs

Retail CBDCs are digital currencies issued directly to the general public. They function as a digital equivalent of physical cash, allowing individuals and businesses to hold and transact in central bank money. The primary goals of retail CBDCs are to enhance financial inclusion, reduce the cost of cash management, and provide a safe, state-backed alternative to private digital currencies and stablecoins.

Wholesale CBDCs

Wholesale CBDCs, on the other hand, are restricted to use by financial institutions, such as commercial banks and clearinghouses. They are designed to facilitate interbank settlements, cross-border payments, and the clearing of large-value transactions. Wholesale CBDCs aim to improve the efficiency, speed, and security of the financial system’s backend infrastructure, reducing counterparty risk and settlement times.

---

African Central Bank Priorities: A Dual Approach

African central banks are adopting diverse strategies based on their unique economic contexts, financial infrastructure maturity, and policy objectives. While some prioritize retail CBDCs to address financial inclusion, others focus on wholesale CBDCs to optimize interbank and cross-border settlements.

The Push for Retail CBDCs: Financial Inclusion and Cashless Economies

For many African nations, financial inclusion remains a pressing challenge. According to the World Bank, a significant portion of the continent’s population remains unbanked or underbanked. Retail CBDCs offer a potential solution by providing a low-cost, accessible digital payment method that does not require a traditional bank account.

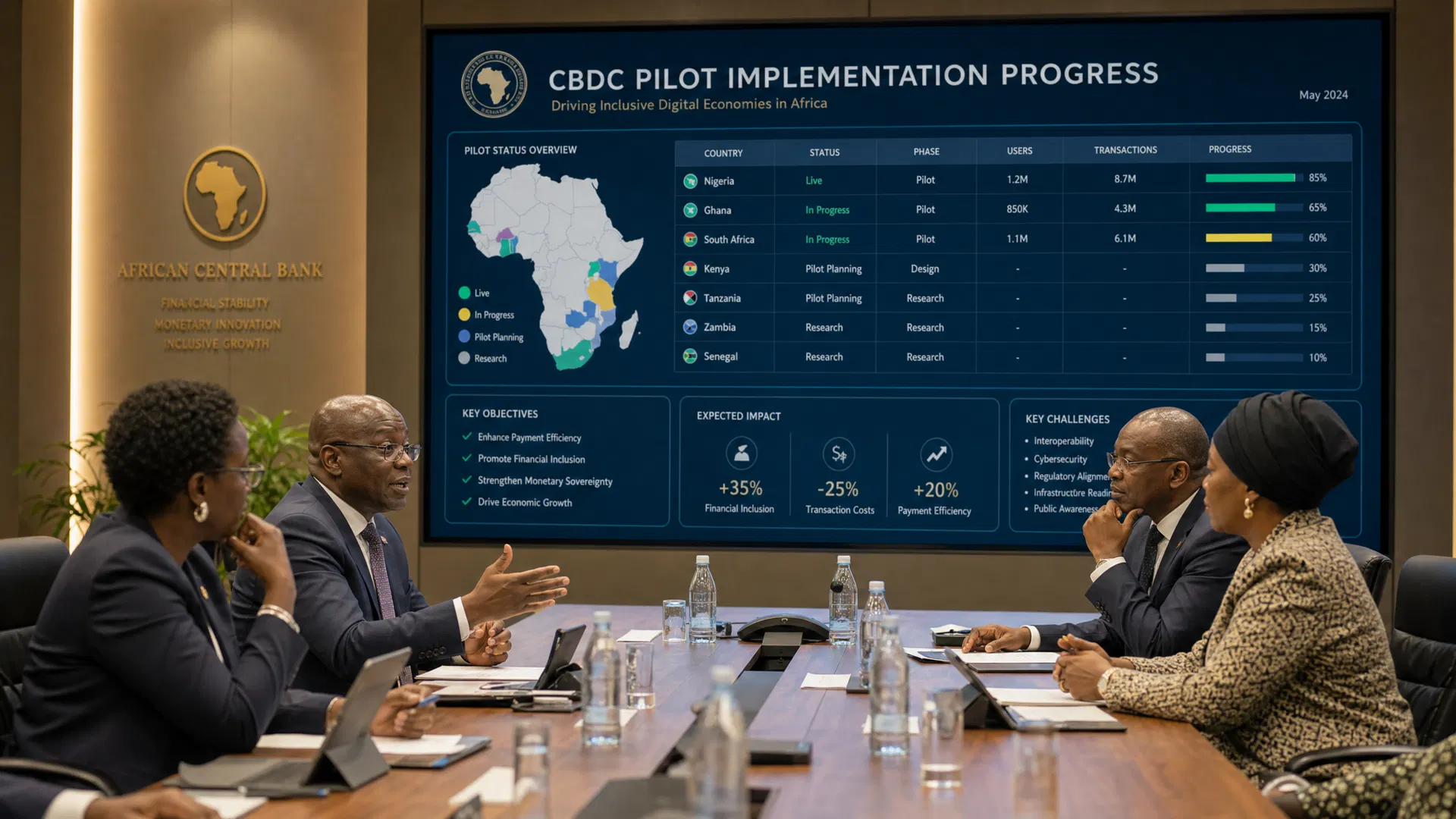

Nigeria’s eNaira: Nigeria, Africa’s largest economy, launched the eNaira in October 2021, becoming the first African country to introduce a retail CBDC. The Central Bank of Nigeria (CBN) prioritized the eNaira to boost financial inclusion, facilitate easier cross-border remittances, and improve the efficiency of welfare payments. Despite initial adoption challenges, the eNaira highlights a strong commitment to retail-focused digital monetary policy.

Ghana’s eCedi: The Bank of Ghana is actively piloting the eCedi, a retail CBDC designed to complement the country’s successful mobile money ecosystem. The eCedi aims to facilitate offline transactions, a critical feature for rural areas with limited internet connectivity, thereby driving deeper financial inclusion.

The Case for Wholesale CBDCs: Efficiency and Cross-Border Trade

In contrast, countries with more developed financial infrastructures are exploring wholesale CBDCs to enhance systemic efficiency and support regional trade integration.

South Africa’s Project Khokha: The South African Reserve Bank (SARB) has been a pioneer in wholesale CBDC research through Project Khokha. The initiative successfully demonstrated how a wholesale CBDC, utilizing distributed ledger technology (DLT), could expedite interbank settlements and reduce systemic risk. South Africa’s focus reflects its position as a regional financial hub, prioritizing the modernization of wholesale financial markets.

Cross-Border Initiatives: Wholesale CBDCs are also gaining traction as a tool to facilitate cross-border payments, a historical pain point in intra-African trade. Initiatives like the Pan-African Payment and Settlement System (PAPSS) could potentially integrate with wholesale CBDCs to streamline currency conversions and reduce reliance on correspondent banking networks, supporting the goals of the African Continental Free Trade Area (AfCFTA).

---

Strategic Considerations for Policymakers and Investors

The divergence in CBDC priorities across Africa presents both opportunities and challenges for the digital finance ecosystem.

- Infrastructure Readiness: The successful deployment of either retail or wholesale CBDCs requires robust digital infrastructure, including reliable internet access, cybersecurity frameworks, and interoperable payment systems. Policymakers must align their CBDC ambitions with their infrastructural capabilities.

- Regulatory Harmonization: As African nations develop distinct CBDC models, regional regulatory harmonization will be critical to ensure interoperability, particularly for cross-border trade and remittances.

- Public-Private Partnerships: Central banks cannot build the CBDC ecosystem in isolation. Collaboration with commercial banks, fintech companies, and mobile network operators is essential to drive adoption and innovation, particularly for retail CBDCs.

---

Conclusion

The choice between retail and wholesale CBDCs in Africa is not a binary one; rather, it reflects the diverse economic priorities of individual nations. While retail CBDCs hold the promise of bringing millions into the formal financial system, wholesale CBDCs offer the potential to revolutionize interbank settlements and cross-border trade. As African central banks continue to pilot and deploy these digital currencies, their strategic choices will profoundly shape the continent’s digital monetary future, offering compelling opportunities for institutional investors and shaping the next era of African digital finance.