Introduction to the IMF CBDC Guidelines and Africa's Digital Transformation

The International Monetary Fund (IMF) has increasingly recognized the transformative potential of Central Bank Digital Currencies (CBDCs) in reshaping the global financial architecture. As digital assets and tokenized ecosystems gain unprecedented traction, the IMF has proactively developed comprehensive guidelines to assist central banks in navigating the complexities of CBDC design, issuance, and regulation. For the African continent, which stands at the precipice of a digital economy revolution, these guidelines offer a critical blueprint. African central banks are actively exploring, piloting, and implementing digital currency frameworks to enhance financial inclusion, streamline cross-border payments, and modernize sovereign digital asset infrastructure.

The IMF's approach to CBDCs emphasizes the necessity of robust macroeconomic stability, financial integrity, and consumer protection. By providing a structured methodology for evaluating the feasibility of digital currencies, the IMF aims to mitigate risks associated with rapid technological adoption. In Africa, where mobile money has demonstrated immense demand for accessible digital financial services, central banks are leveraging the IMF's insights to design CBDCs that complement existing payment systems while addressing systemic inefficiencies. As platforms like AfriVest build the continent's sovereign digital asset infrastructure, aligning with these international standards is paramount for ensuring interoperability, security, and regulatory compliance across diverse jurisdictions.

Key Provisions of the IMF CBDC Frameworks

The IMF's CBDC guidelines articulate foundational principles that central banks must consider when developing digital currency ecosystems. Foremost among these is the imperative of maintaining monetary policy efficacy and financial stability. The IMF advises central banks to carefully calibrate the design features of CBDCs, such as remuneration and holding limits, to prevent the disintermediation of commercial banks and the potential destabilization of the traditional financial sector. Furthermore, the guidelines stress the importance of technological resilience, urging central banks to adopt scalable, secure, and interoperable infrastructures that can withstand cyber threats and operational disruptions.

Another critical provision within the IMF frameworks is the emphasis on legal and regulatory clarity. The issuance of a CBDC requires a robust legal foundation that explicitly defines the legal tender status of the digital currency, the rights and obligations of users, and the regulatory oversight mechanisms. The IMF also highlights the necessity of integrating comprehensive Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) controls into the CBDC architecture.

African Central Banks' Response and Regulatory Adaptation

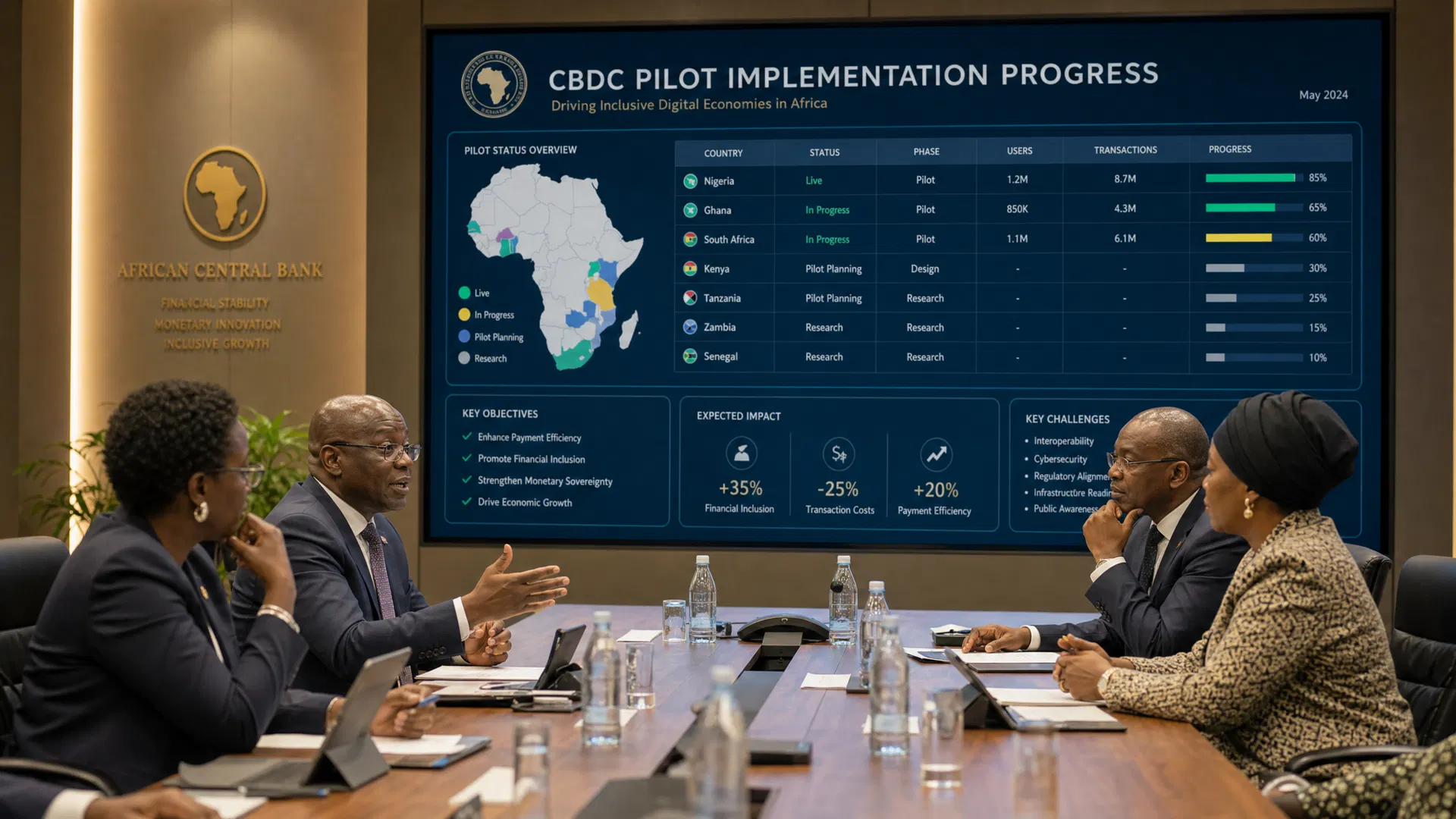

Across the African continent, central banks are responding to the IMF's CBDC guidelines with varying degrees of urgency and innovation. The Central Bank of Nigeria (CBN), a pioneer in this domain, launched the eNaira in October 2021, becoming one of the first central banks globally to issue a retail CBDC. Similarly, the South African Reserve Bank (SARB) has engaged in extensive research and pilot programs, notably Project Khokha, which explores the use of distributed ledger technology for wholesale payment systems and interbank settlements.

Other nations, including Ghana, Kenya, and Rwanda, are also advancing their CBDC explorations. The Bank of Ghana's eCedi pilot emphasizes offline functionality to cater to unbanked populations in remote areas, directly addressing the IMF's focus on inclusive design. Meanwhile, the Central Bank of Kenya has published discussion papers soliciting public and industry feedback on the potential issuance of a digital shilling. As these central banks navigate the complexities of CBDC implementation, they are simultaneously updating their regulatory frameworks to accommodate digital assets. This includes harmonizing domestic laws with regional data protection regulations, such as the Protection of Personal Information Act (POPIA) in South Africa, the Data Protection Act (DPA) in Kenya, and the Malabo Convention, ensuring that digital currency ecosystems are both innovative and secure.

Compliance Implications for Digital Asset Platforms

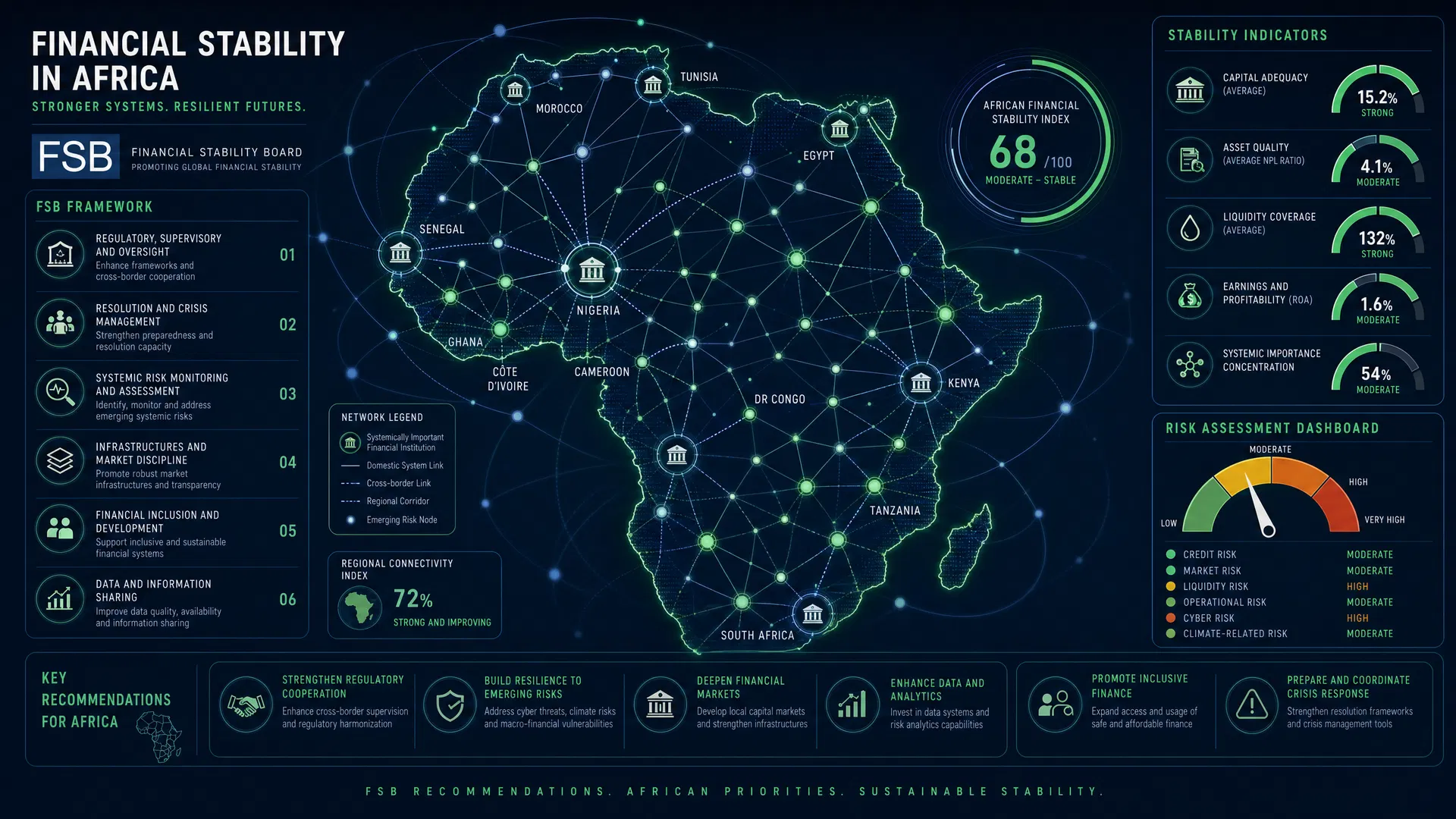

The convergence of IMF CBDC guidelines and evolving African regulatory frameworks introduces significant compliance implications for digital asset platforms and fintech operators. As central banks establish the foundational infrastructure for sovereign digital currencies, private sector participants must ensure that their platforms are fully interoperable and compliant with these emerging standards. For infrastructure providers like AfriVest, this necessitates a meticulous alignment with international protocols, including ISO 20022 for financial messaging, as well as adherence to the regulatory expectations set forth by the International Organization of Securities Commissions (IOSCO) and the Financial Stability Board (FSB).

Compliance in this dynamic environment extends beyond technical interoperability; it requires a comprehensive approach to risk management and legal adherence. Digital asset platforms must implement robust AML/CFT frameworks that integrate seamlessly with central bank infrastructures, enabling real-time transaction monitoring and reporting. Furthermore, the stringent data protection laws across African jurisdictions mandate that platforms adopt privacy-by-design principles. Navigating the intricacies of the Nigeria Data Protection Act (NDPA), the PDPA in Rwanda, and the DPA in Uganda requires sophisticated data governance architectures that ensure the secure processing and localization of user information.

Conclusion: Shaping Africa's Digital Economy Transformation

The integration of IMF CBDC guidelines into the regulatory frameworks of African central banks marks a pivotal moment in the continent's digital economy transformation. By adopting these international standards, African nations are not only modernizing their sovereign financial infrastructures but also positioning themselves as competitive participants in the global digital asset ecosystem. The careful calibration of CBDC design, coupled with robust compliance and enforcement mechanisms, provides a secure and scalable foundation for future financial innovation.

For platforms like AfriVest, the evolving regulatory landscape presents a unique opportunity to build resilient, interoperable, and inclusive digital asset infrastructures. By aligning with the strategic imperatives of African central banks and adhering to rigorous international and regional standards, fintech operators can drive the next wave of economic growth and financial inclusion. As the continent continues to embrace tokenization, digital identity, and sovereign digital currencies, the collaborative efforts of policymakers, regulators, and industry leaders will be instrumental in realizing the full potential of Africa's digital transformation.