Central Bank Digital Currencies in Africa: Regulatory Progress and Implementation Challenges

Central Bank Digital Currencies (CBDCs) represent a transformative frontier in Africa's financial landscape, promising enhanced payment efficiency, financial inclusion, and sovereign monetary sovereignty. As African nations progressively explore and pilot CBDCs, the regulatory frameworks governing their issuance and operation have become critical to ensuring stability, compliance, and interoperability. This article examines the regulatory progress of CBDCs across Africa, the key legal provisions shaping their deployment, compliance imperatives for stakeholders, enforcement mechanisms, and strategic considerations for digital asset platforms such as AfriVest.

Regulatory Background and Institutional Frameworks

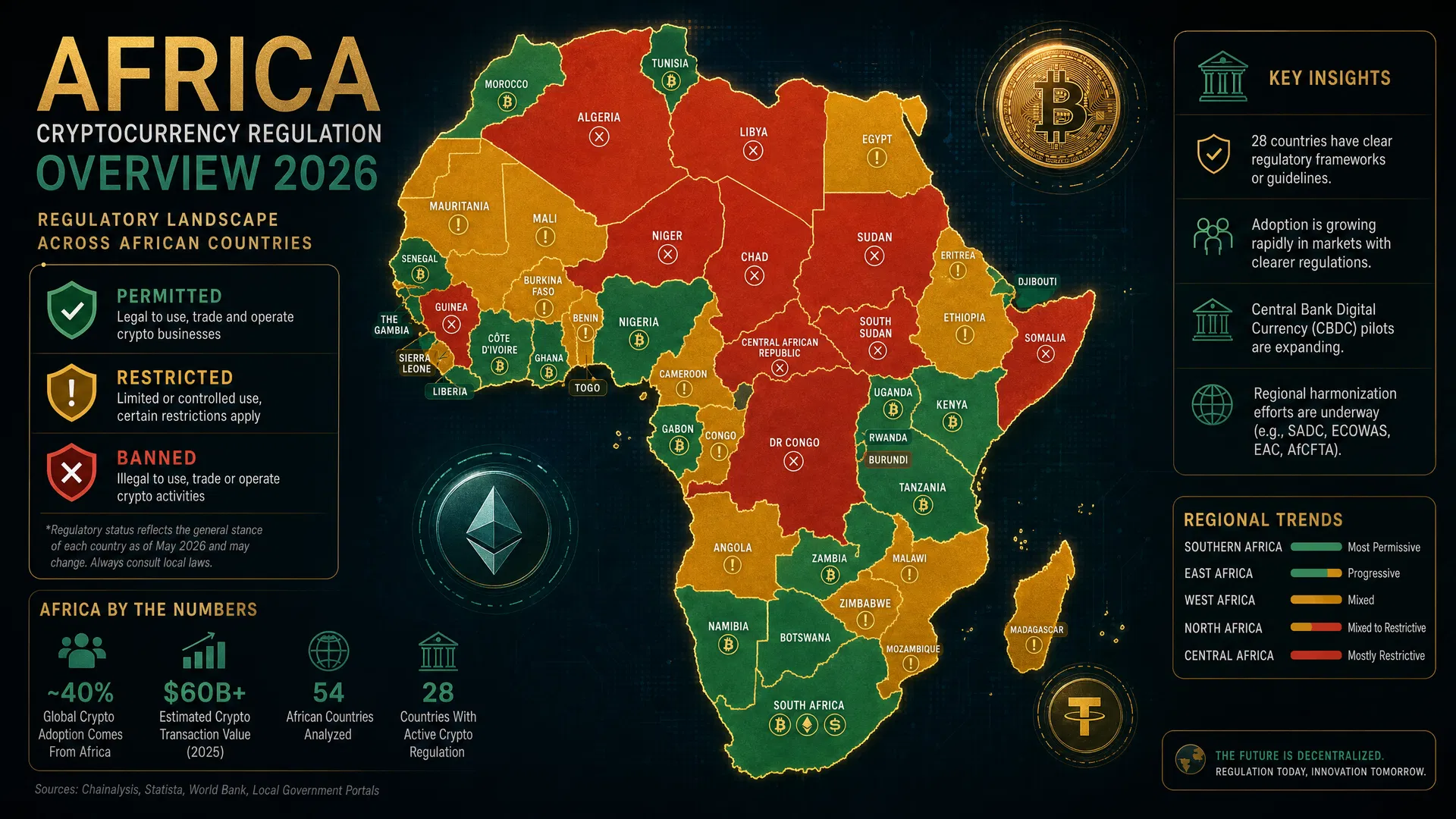

The regulatory evolution of CBDCs in Africa is nested within broader efforts to modernize financial systems, harmonize digital finance regulations, and align with international standards. The Central Bank of Nigeria (CBN) pioneered Africa’s first sovereign CBDC, the eNaira, launched in October 2021 under the regulatory purview of the Central Bank of Nigeria Act (2007) and the Currency and Exchange Act. Similarly, the South African Reserve Bank (SARB) initiated the Project Khokha CBDC pilot in 2020, guided by the SARB Act (1989) and the Financial Sector Regulation Act (2017).

Beyond individual initiatives, regional regulatory coherence is advancing. The African Union’s Malabo Convention (2014) on Cyber Security and Personal Data Protection influences data governance for digital currencies, while regional data protection laws—such as South Africa’s Protection of Personal Information Act (POPIA, 2013), Kenya’s Data Protection Act (2019), and Ghana’s Data Protection Act (2012)—ensure that CBDCs comply with privacy and data security requirements. Internationally, African regulators increasingly reference frameworks from the Financial Action Task Force (FATF), the International Monetary Fund (IMF) CBDC guidelines (2020), the Financial Stability Board (FSB), and ISO 20022 messaging standards for payment interoperability.

Key Provisions in CBDC Legislation

CBDC-related legislation in Africa primarily addresses legal tender status, issuance authority, operational scope, and consumer protection. For example, Nigeria’s eNaira Provisional Regulations (2021) affirm the eNaira as legal tender, stipulate that the CBN retains exclusive issuance rights, and mandate KYC/AML compliance aligned with the Money Laundering (Prohibition) Act (2011). Similarly, Ghana’s Bank of Ghana Act (2002), amended in 2021 to support digital currency frameworks, codifies the Bank of Ghana’s authority to issue e-Cedi and requires adherence to AML/CFT standards consistent with FATF recommendations.

Moreover, CBDC frameworks emphasize interoperability with existing payment systems and cross-border functionality, reflecting provisions in the East African Community Payments System Act (2019). Data protection clauses safeguard user information under regional laws such as Nigeria’s NDPR (2019) and Kenya’s Data Protection Act. These provisions collectively establish a legal architecture balancing innovation with systemic risk mitigation.

Compliance Implications for Institutional Stakeholders

Compliance with CBDC regulations necessitates integrated governance mechanisms for financial institutions, fintech operators, and digital asset platforms. Institutional investors must ensure that CBDC holdings and transactions conform to AML/CFT protocols under the FATF’s revised Recommendations (2023). Digital identity systems linked to CBDCs require strict adherence to identity verification standards, echoing AfriVest’s alignment with ISO 20022 and regional data privacy laws.

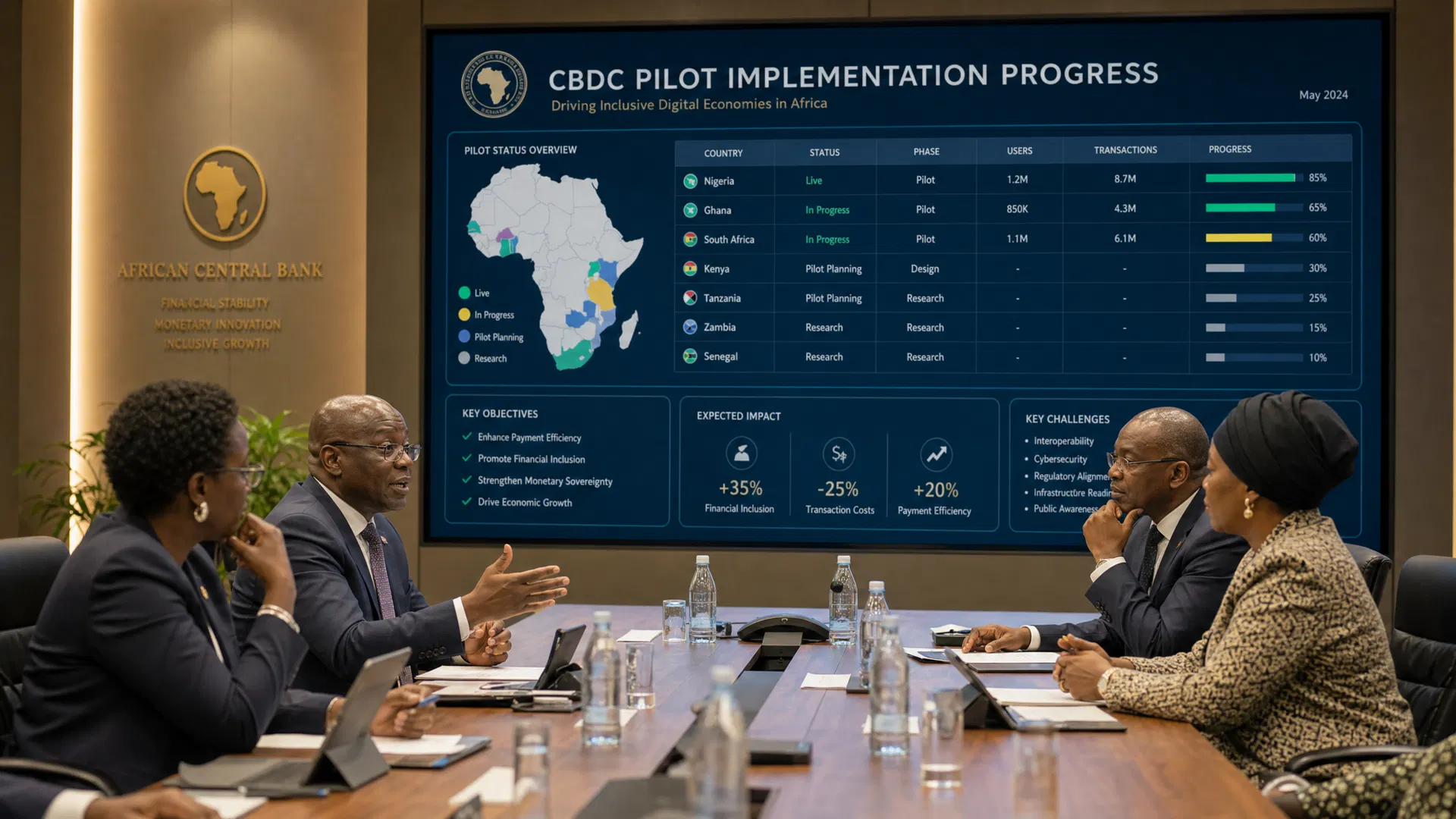

Furthermore, fintech operators facilitating CBDC interoperability and tokenization must implement robust cybersecurity controls, contingency planning, and transaction monitoring to comply with prudential directives issued by respective central banks. For example, the Bank of Uganda’s CBDC pilot guidelines (2022) mandate real-time transaction reporting and audit trails, underscoring the importance of transparent record-keeping for regulatory scrutiny.

Enforcement Mechanisms and Regulatory Oversight

Enforcement of CBDC regulations in Africa is primarily the remit of central banks supported by financial intelligence units (FIUs) and data protection authorities. The CBN, for instance, can impose sanctions, including fines or operational suspensions, under the Central Bank of Nigeria Act for non-compliance with eNaira regulations. Similarly, South Africa’s Financial Sector Conduct Authority (FSCA) monitors adherence to SARB’s CBDC pilot parameters, with enforcement powers under the Financial Sector Regulation Act.

Cross-border enforcement challenges persist due to jurisdictional complexities, necessitating cooperation frameworks such as the African Financial Intelligence Units Network (AFIN). The evolving regulatory landscape also anticipates enhanced supervisory technologies (SupTech) to detect illicit activities and systemic risks, aligning with the OECD’s 2022 recommendations on digital finance supervision.

Preparing Digital Asset Platforms for CBDC Integration

Digital asset infrastructure providers like AfriVest must proactively adapt to regulatory expectations by embedding compliance-by-design principles. This includes integrating multi-jurisdictional data privacy compliance modules, supporting ISO 20022 messaging for seamless CBDC interoperability, and enabling secure digital identity verification aligned with FATF and IMF standards.

Platforms should also prioritize scalability and modular architecture to accommodate evolving central bank requirements and facilitate cooperative frameworks with cooperatives and stablecoin operators. Engaging with regulators through sandbox initiatives and public-private dialogues will be essential to anticipate regulatory shifts and operationalize compliant CBDC solutions.

Conclusion: Advancing Africa’s Digital Economy through CBDC Regulation

Africa’s progress in CBDC regulation marks a critical step toward a more inclusive, efficient, and secure digital economy. While regulatory frameworks are maturing, challenges remain in harmonizing standards across diverse jurisdictions, enforcing compliance effectively, and fostering innovation without compromising financial stability. Digital asset platforms equipped with robust regulatory intelligence and interoperable infrastructure will play a pivotal role in operationalizing sovereign digital currencies, thereby accelerating Africa’s transformation into a leading digital finance hub. The convergence of regional laws, international standards, and technological innovation positions Africa to redefine monetary sovereignty and financial inclusion through well-regulated CBDC ecosystems.