Introduction: The Maturing Landscape of African Digital Assets

The African continent has emerged as a dynamic frontier for digital asset adoption, driven by demographic dividends, mobile money penetration, and the necessity for efficient cross-border payment solutions. As of 2026, the regulatory environment across the continent has transitioned from cautious observation to proactive framework development. Institutional investors, policymakers, and fintech operators are navigating a complex mosaic of national regulations that seek to balance financial innovation with systemic stability and consumer protection. For platforms like AfriVest, which are building sovereign digital asset infrastructure encompassing tokenization, central bank digital currencies (CBDCs), and stablecoins, understanding this evolving landscape is paramount. The alignment of national frameworks with international standards, such as those promulgated by the Financial Action Task Force (FATF), the International Organization of Securities Commissions (IOSCO), and the Financial Stability Board (FSB), underscores a collective drive toward regulatory harmonization and global integration.

Regulatory Background and Key Provisions Across Major Jurisdictions

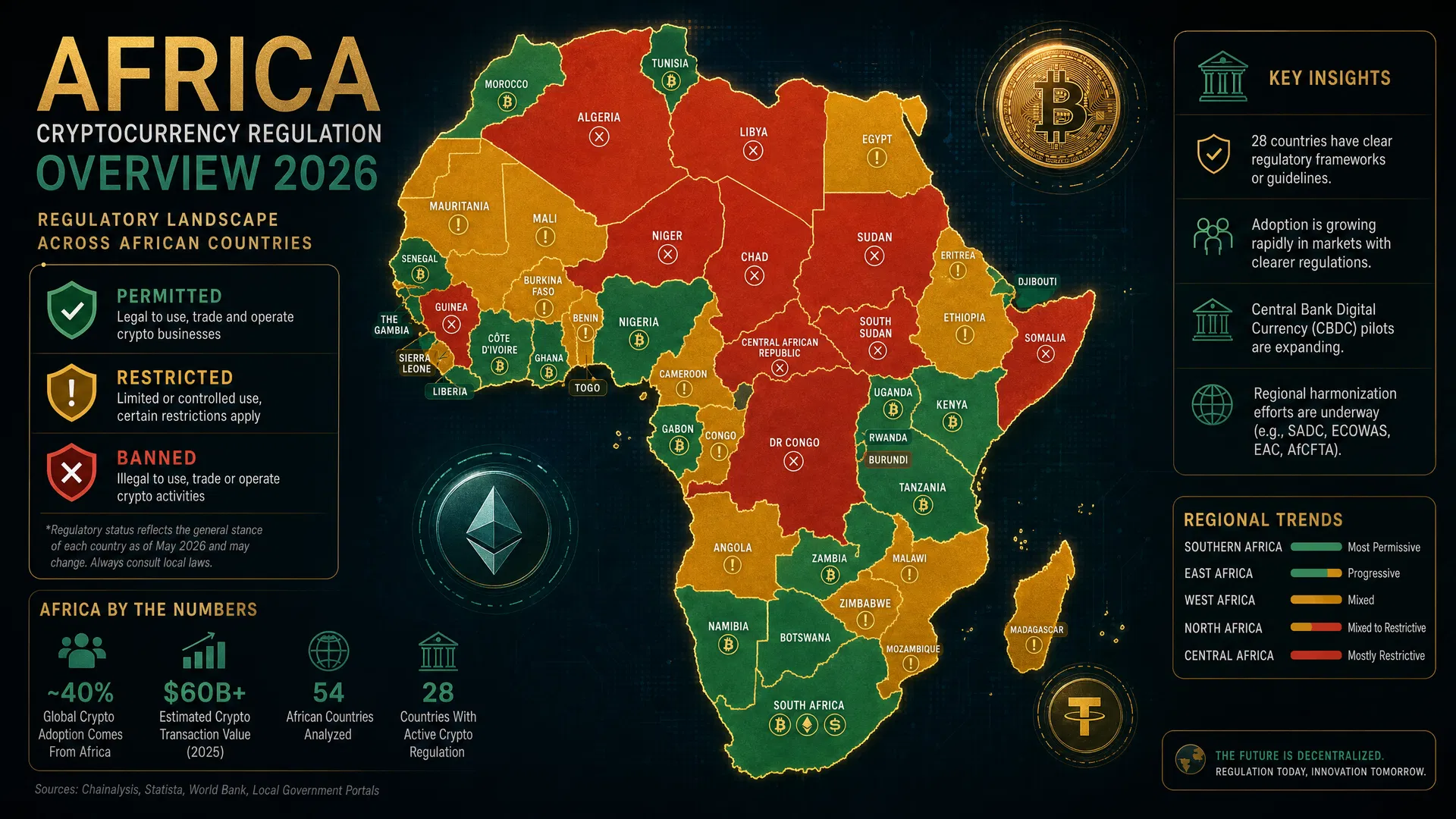

The regulatory trajectory in Africa is characterized by distinct approaches tailored to specific macroeconomic contexts. In South Africa, the Financial Sector Conduct Authority (FSCA) formally declared crypto assets as financial products under the Financial Advisory and Intermediary Services (FAIS) Act in 2022, setting a precedent for comprehensive oversight. By 2026, the regulatory framework has matured to mandate stringent licensing requirements for Crypto Asset Service Providers (CASPs), enforcing rigorous Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) protocols. Similarly, Nigeria has shifted from its initial restrictive stance to a more structured regulatory environment. The Securities and Exchange Commission (SEC) of Nigeria has implemented rules on digital asset issuance, offering platforms, and custody, requiring virtual asset service providers to register and comply with capital adequacy and disclosure norms.

In East Africa, Kenya has advanced its regulatory posture through the Capital Markets Authority (CMA), which has introduced sandbox environments to test digital asset innovations while formulating definitive guidelines. The focus remains heavily on consumer protection and mitigating risks associated with market volatility. Meanwhile, Mauritius continues to position itself as a progressive hub, leveraging its Virtual Asset and Initial Token Offering Services (VAITOS) Act of 2021. The Financial Services Commission (FSC) of Mauritius enforces a comprehensive licensing regime that categorizes virtual asset service providers, ensuring robust governance, risk management, and compliance with international AML/CFT standards. These diverse regulatory approaches highlight the necessity for digital asset platforms to adopt adaptable and localized compliance strategies.

Compliance Implications and Data Protection Mandates

The intersection of digital asset regulation and data privacy is a critical compliance frontier for operators in Africa. The proliferation of digital identity solutions and tokenized assets necessitates strict adherence to regional and national data protection laws. South Africa's Protection of Personal Information Act (POPIA) and the Nigeria Data Protection Act (NDPA) impose rigorous obligations on data controllers and processors regarding the collection, storage, and cross-border transfer of personal data. Furthermore, the harmonization of data privacy standards is increasingly influenced by regional frameworks such as the Malabo Convention, which advocates for robust cybersecurity and personal data protection across the African Union.

For digital asset platforms, these mandates require the implementation of privacy-by-design architectures. Compliance implications extend to the management of decentralized ledgers, where the immutability of blockchain technology must be reconciled with the right to erasure and data minimization principles enshrined in laws like the Data Protection Act of Kenya and the Data Protection and Privacy Act of Uganda. Platforms must deploy advanced cryptographic techniques, such as zero-knowledge proofs, to facilitate verifiable transactions without compromising user privacy. The integration of ISO 20022 messaging standards further ensures that data transmitted across financial networks is structured, secure, and compliant with both financial and privacy regulations.

Enforcement Mechanisms and Supervisory Oversight

Regulatory authorities across Africa are increasingly equipping themselves with advanced supervisory technologies (SupTech) to monitor digital asset markets and enforce compliance. The deployment of blockchain analytics tools enables regulators to trace illicit financial flows, monitor transaction typologies, and ensure adherence to FATF's Travel Rule. In jurisdictions like South Africa and Mauritius, regulatory bodies conduct regular thematic reviews and on-site inspections of licensed entities to assess the adequacy of their AML/CFT frameworks and operational resilience.

Enforcement mechanisms are becoming more stringent, with regulators imposing substantial administrative penalties, suspending licenses, and initiating criminal proceedings against non-compliant operators. The collaborative efforts between financial regulators, central banks, and law enforcement agencies are critical in mitigating systemic risks. For instance, the Inter-Governmental Action Group against Money Laundering in West Africa (GIABA) plays a pivotal role in coordinating regional AML/CFT initiatives and ensuring that member states implement robust enforcement frameworks. Digital asset platforms must proactively engage with regulators, participate in industry associations, and maintain transparent reporting mechanisms to navigate the heightened supervisory environment successfully.

Conclusion: Driving Africa's Digital Economy Transformation

The regulatory maturation of cryptocurrency and digital assets in Africa represents a pivotal milestone in the continent's digital economy transformation. As national frameworks increasingly align with global standards, the foundation is being laid for a secure, inclusive, and interoperable financial ecosystem. The transition from fragmented oversight to structured regulatory regimes provides the clarity necessary for institutional investment and sustainable innovation. For infrastructure platforms like AfriVest, the ability to navigate this complex regulatory mosaic is not merely a compliance obligation but a strategic imperative. By embedding robust governance, data protection, and AML/CFT protocols into their core architecture, digital asset platforms will play a catalytic role in unlocking Africa's economic potential, fostering financial inclusion, and integrating the continent into the global digital economy.