The Current Landscape of African Cross-Border Transactions

The African continent is experiencing a profound transformation in its digital economy, driven by rapid mobile penetration. Despite these advancements, cross-border payments remain a significant challenge hindering intra-African trade. Historically, the financial architecture across the continent has been highly fragmented, relying on legacy correspondent banking networks that are often inefficient and costly. This fragmentation creates substantial friction for businesses attempting to move capital across borders, ultimately stifling economic growth. Addressing these payment inefficiencies has become a paramount priority for policymakers and financial institutions alike.

The emergence of innovative financial technologies has begun to disrupt this traditional landscape, offering new pathways for seamless capital mobility. Central Bank Digital Currencies (CBDCs) have surfaced as a promising solution to the persistent challenges of cross-border payments. By leveraging sovereign digital currencies, African nations can bypass the cumbersome correspondent banking system and establish direct, real-time settlement mechanisms. This shift promises to reduce transaction times from days to mere seconds while significantly lowering associated costs. The exploration of CBDCs is a strategic imperative for central banks aiming to modernize monetary systems.

The High Cost of Remittance Africa and Structural Bottlenecks

One of the most pressing issues within the current financial paradigm is the exorbitant cost associated with remittance Africa. Sub-Saharan Africa remains the most expensive region globally for sending money, with average transaction fees frequently exceeding eight percent. These prohibitive costs disproportionately affect vulnerable populations, eroding the value of funds critical for household consumption, education, and healthcare. The structural bottlenecks contributing to these high fees include a lack of interoperability between domestic payment systems, stringent foreign exchange controls, and the monopolistic practices of dominant money transfer operators.

Addressing the inefficiencies in remittance flows requires a comprehensive overhaul of the underlying financial infrastructure. Traditional remittance channels are heavily reliant on multiple intermediaries, each extracting a fee and adding delays to the settlement process. By transitioning toward digital currency integration, African nations can streamline these processes, enabling peer-to-peer transfers that circumvent traditional intermediaries. This disintermediation is crucial for driving down costs and ensuring that a larger portion of remitted funds reaches the intended beneficiaries. Furthermore, integrating blockchain technology into remittance corridors offers a compelling solution to transparency and traceability challenges.

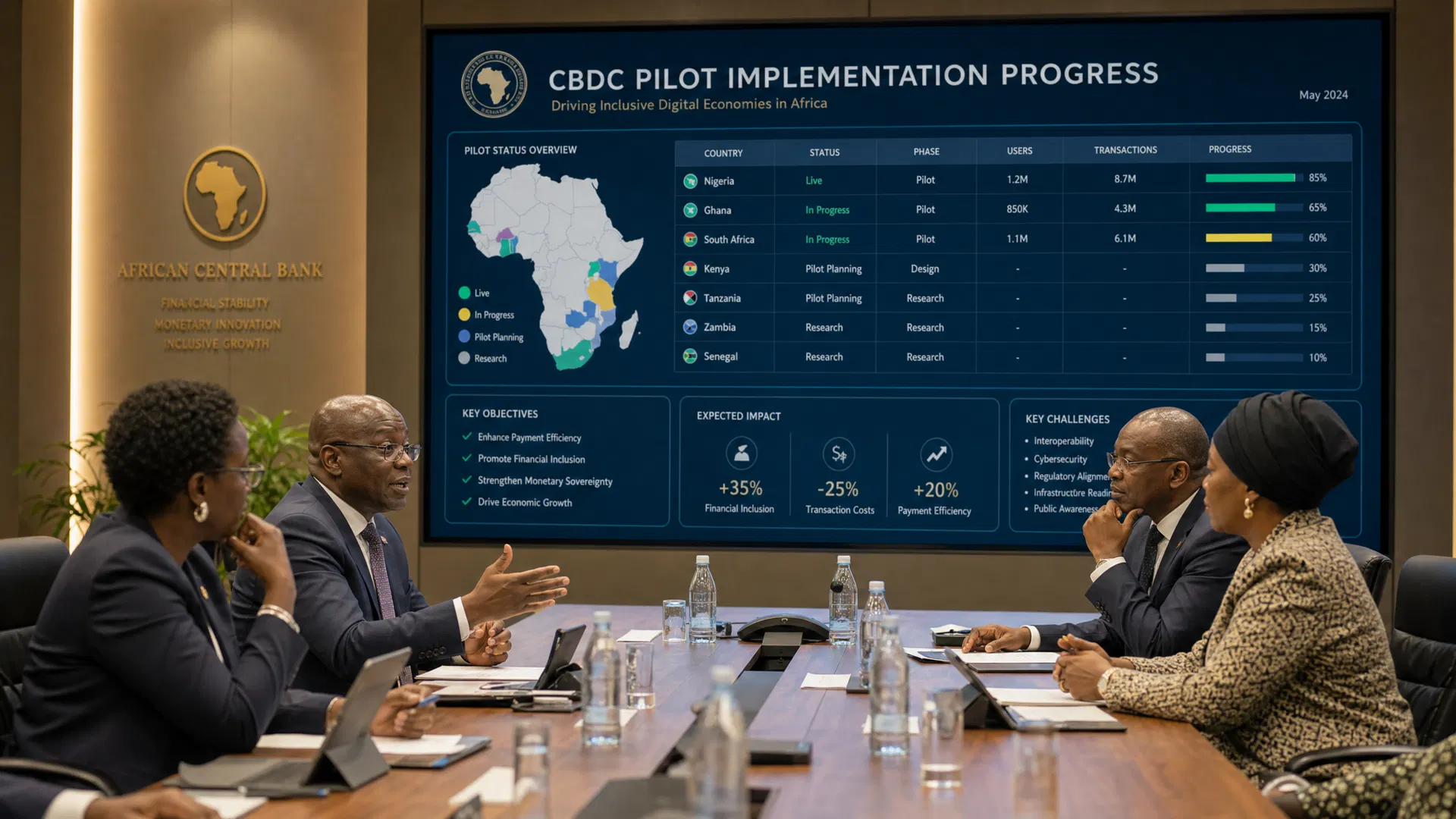

Pan-African CBDC Initiatives: A Catalyst for Financial Integration

The concept of a Pan-African CBDC represents a bold and visionary approach to overcoming the continent's fragmented monetary landscape. While several African nations have made significant strides in developing domestic digital currencies, the true transformative potential lies in cross-border interoperability. A coordinated Pan-African CBDC framework could serve as the ultimate catalyst for financial integration, facilitating seamless transactions across diverse jurisdictions without the need for complex currency conversions. This unified approach aligns perfectly with the objectives of the AfCFTA, providing the essential digital payment backbone required to support a single continental market.

Developing a cohesive Pan-African CBDC strategy necessitates unprecedented collaboration among regional central banks, regulatory authorities, and private sector stakeholders. The design of such a system must prioritize interoperability, ensuring that domestic digital currencies can communicate and settle transactions efficiently across borders. Initiatives like the Pan-African Payment and Settlement System have already laid the groundwork for regional financial integration, demonstrating the viability of localized settlement mechanisms. By building upon these existing frameworks and incorporating CBDC capabilities, policymakers can create a highly resilient and scalable payment infrastructure tailored to the unique economic realities of Africa.

Upgrading Financial Infrastructure for the Digital Economy

To fully capitalize on the opportunities presented by CBDCs, Africa must prioritize the comprehensive upgrading of its underlying financial infrastructure. The current legacy systems, characterized by siloed databases and outdated messaging protocols, are ill-equipped to handle the volume and velocity of transactions demanded by a modern digital economy. Investing in next-generation financial infrastructure is essential for supporting the high-throughput, low-latency requirements of digital currency networks. This modernization effort encompasses not only the core settlement engines but also peripheral systems, including digital identity verification, cybersecurity frameworks, and application programming interfaces that enable open banking.

The modernization of financial infrastructure also presents a unique opportunity to bridge the financial inclusion gap that persists across much of the continent. By designing digital payment systems accessible via basic mobile devices, policymakers can extend financial services to unbanked populations. This inclusive approach ensures that the benefits of digital transformation are distributed equitably, empowering marginalized communities to participate actively in the formal economy. Public-private partnerships will play a pivotal role in financing and executing these ambitious infrastructure projects, pooling resources and expertise to accelerate the deployment of world-class financial systems.

Conclusion: Forging a Unified Digital Financial Future

The intersection of cross-border payments and CBDCs represents a generational opportunity to redefine the economic trajectory of the African continent. By embracing digital currency integration and leveraging the transformative power of blockchain technology, African nations can dismantle the historical barriers that have long impeded intra-regional trade and financial inclusion. The transition toward a unified, efficient, and secure payment ecosystem is not merely a technological upgrade; it is a strategic imperative for realizing the full potential of the African Continental Free Trade Area and establishing the continent as a formidable player globally. This evolution is essential for fostering a more inclusive and dynamic economic environment.

As policymakers and institutional investors navigate this landscape, a steadfast commitment to collaboration and regulatory harmonization is essential. The development of a Pan-African CBDC framework, coupled with targeted investments in modernized financial infrastructure, will unlock unprecedented economic value. Such collaborative efforts ensure that the benefits of digital innovation are widely shared. Ultimately, by seizing this pan-African opportunity, the continent can forge a resilient digital financial future, empowering its citizens and businesses to thrive in an interconnected world.