FSB Recommendations and African Financial Stability Mechanisms in the Digital Age

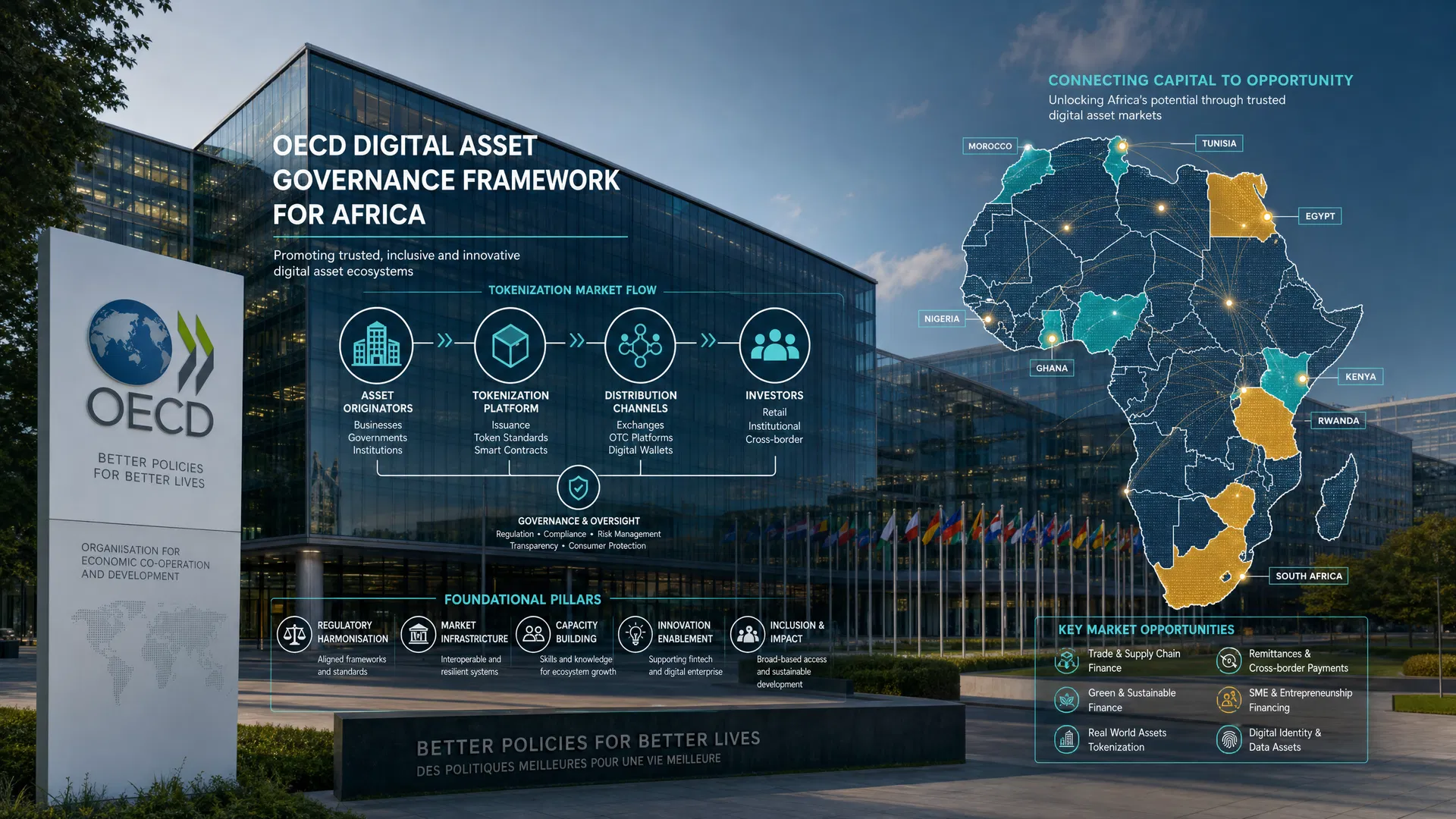

The rapid evolution of digital assets across Africa underscores the necessity for robust financial stability frameworks that align with global standards yet address regional specificities. AfriVest, as Africa’s sovereign digital asset infrastructure platform, operates at the intersection of innovation and regulation, building comprehensive systems encompassing tokenization, CBDC infrastructure, digital identity, stablecoins, and financial inclusion. This article examines the Financial Stability Board’s (FSB) recommendations on digital assets, African financial stability mechanisms, and the implications for digital asset platforms poised to drive Africa’s digital economy.

Regulatory Background: Global Standards and African Context

The Financial Stability Board (FSB), established in 2009 by the G20, plays a critical role in coordinating international financial regulation to promote global financial stability. In October 2020, the FSB released its “Regulatory, Supervisory and Oversight Issues Relating to Crypto-Asset Activities” report, highlighting the risks that crypto-assets may pose to financial stability, consumer protection, and market integrity. The FSB’s updated guidance in July 2023 emphasizes the need for comprehensive regulatory frameworks, covering stablecoins, decentralized finance (DeFi), and the cross-border nature of digital assets.

Africa’s regulatory landscape is shaped by a combination of regional and national laws that address data protection, digital finance, and monetary policy. Key legislative frameworks include South Africa’s Protection of Personal Information Act (POPIA, 2013), Kenya’s Data Protection Act (DPA, 2019), Ghana’s Data Protection Act (2012), Rwanda’s Personal Data Protection Act (PDPA, 2021), Uganda’s Data Protection and Privacy Act (DPA, 2019), Zimbabwe’s Data Protection Act (2021), and the Malabo Convention on Cybersecurity and Personal Data Protection (2014). These laws complement international standards such as ISO 20022 for financial messaging, FATF’s 2019 updated Recommendations on virtual assets, IOSCO’s principles on crypto-asset trading platforms, and the IMF’s 2021 CBDC framework.

Key Provisions of the FSB Recommendations

The FSB emphasizes several core provisions to mitigate risks associated with digital assets. These include:

- Regulatory Clarity and Coordination: Jurisdictions must clearly define regulatory mandates for digital asset activities and ensure coordination among central banks, securities regulators, and anti-money laundering bodies.

- Risk Management Requirements: Digital asset platforms should implement robust risk management frameworks addressing operational, cyber, liquidity, and market risks.

- Stablecoin Oversight: Given stablecoins’ potential systemic impact, the FSB advocates for prudential regulation similar to that applied to traditional payment systems and banking institutions.

- Cross-border Cooperation: Recognizing the inherently global nature of digital assets, the FSB calls for enhanced international cooperation on supervision, enforcement, and information sharing.

- Consumer and Investor Protection: Transparency and disclosure requirements are critical, alongside mechanisms to prevent fraud, market manipulation, and ensure redress.

- Anti-Money Laundering and Counter-Terrorist Financing (AML/CFT): Alignment with FATF’s updated Recommendations is essential, including customer due diligence and reporting obligations.

Compliance Implications for African Digital Asset Platforms

For African digital asset platforms like AfriVest, compliance with FSB recommendations involves integrating international best practices within Africa’s heterogeneous regulatory environment. Platforms must reconcile global standards with regional data protection laws, such as POPIA, Kenya’s DPA, and the Malabo Convention, which impose stringent requirements on personal data processing, consent, and cross-border transfers.

Implementing ISO 20022 standards facilitates interoperability and efficient messaging across payment systems, which is critical for CBDC infrastructure and tokenization efforts. Alignment with FATF’s virtual asset guidelines mandates comprehensive AML/CFT controls, including customer identification and suspicious transaction reporting, which is increasingly scrutinized by African Financial Intelligence Units (FIUs).

In addition, adherence to IOSCO’s principles for crypto-asset trading platforms ensures market integrity and investor protection, which is vital as institutional investors increase their exposure to African digital assets. The IMF’s CBDC framework further supports central banks in designing resilient, inclusive digital currencies that complement existing financial systems.

Enforcement Mechanisms and Supervisory Frameworks

Enforcement across Africa varies by jurisdiction but is increasingly harmonized through regional bodies such as the African Securities Exchanges Association (ASEA) and the Committee of Central Bank Governors (CCBG). National regulators, including the South African Reserve Bank (SARB), Kenya’s Capital Markets Authority (CMA), and Ghana’s Securities and Exchange Commission (SEC), have begun enforcing digital asset regulations consistent with FSB guidance. Penalties for non-compliance range from fines and license revocations to criminal sanctions under anti-money laundering statutes.

The FSB encourages enhancing supervisory capacities through technological tools like RegTech and SupTech, enabling real-time monitoring of digital asset activities and facilitating cross-border information sharing. The establishment of cooperative supervisory arrangements is critical to address challenges posed by decentralized finance and cross-jurisdictional operations that characterize many digital asset platforms. For example, the East African Community’s (EAC) efforts to harmonize fintech regulations across member states exemplify regional approaches to enforcement.

Preparing Digital Asset Platforms for Regulatory Compliance

Digital asset platforms must adopt a proactive compliance posture to navigate evolving regulatory landscapes effectively. This include:

- Governance and Risk Frameworks: Establishing clear governance structures with dedicated compliance officers and risk management protocols tailored to digital assets.

- Technology Integration: Deploying AML/CFT systems compliant with FATF standards and leveraging ISO 20022 messaging to ensure interoperability and regulatory reporting.

- Data Protection Alignment: Ensuring compliance with regional data protection laws by implementing robust data governance, consent management, and secure data storage solutions.

- Stakeholder Engagement: Engaging regulators, policymakers, and industry bodies to contribute to regulatory development and gain early insights into enforcement trends.

- Capacity Building: Investing in staff training on compliance requirements, emerging risks, and technological innovations such as CBDCs and stablecoins.

Conclusion: Advancing Africa’s Digital Economy Through Resilient Financial Infrastructure

The FSB’s recommendations provide a comprehensive blueprint for managing the complexities and risks posed by digital assets while fostering innovation and inclusion. For Africa, integrating these global standards with regional regulatory frameworks is pivotal to building resilient financial stability mechanisms that underpin sovereign digital asset infrastructure. AfriVest’s commitment to aligning with international standards and regional data protection laws positions it as a catalyst for Africa's digital economy transformation. By embracing regulatory rigor, digital asset platforms can unlock the full potential of tokenization, CBDCs, and stablecoins, driving financial inclusion and sustainable economic growth across the continent.