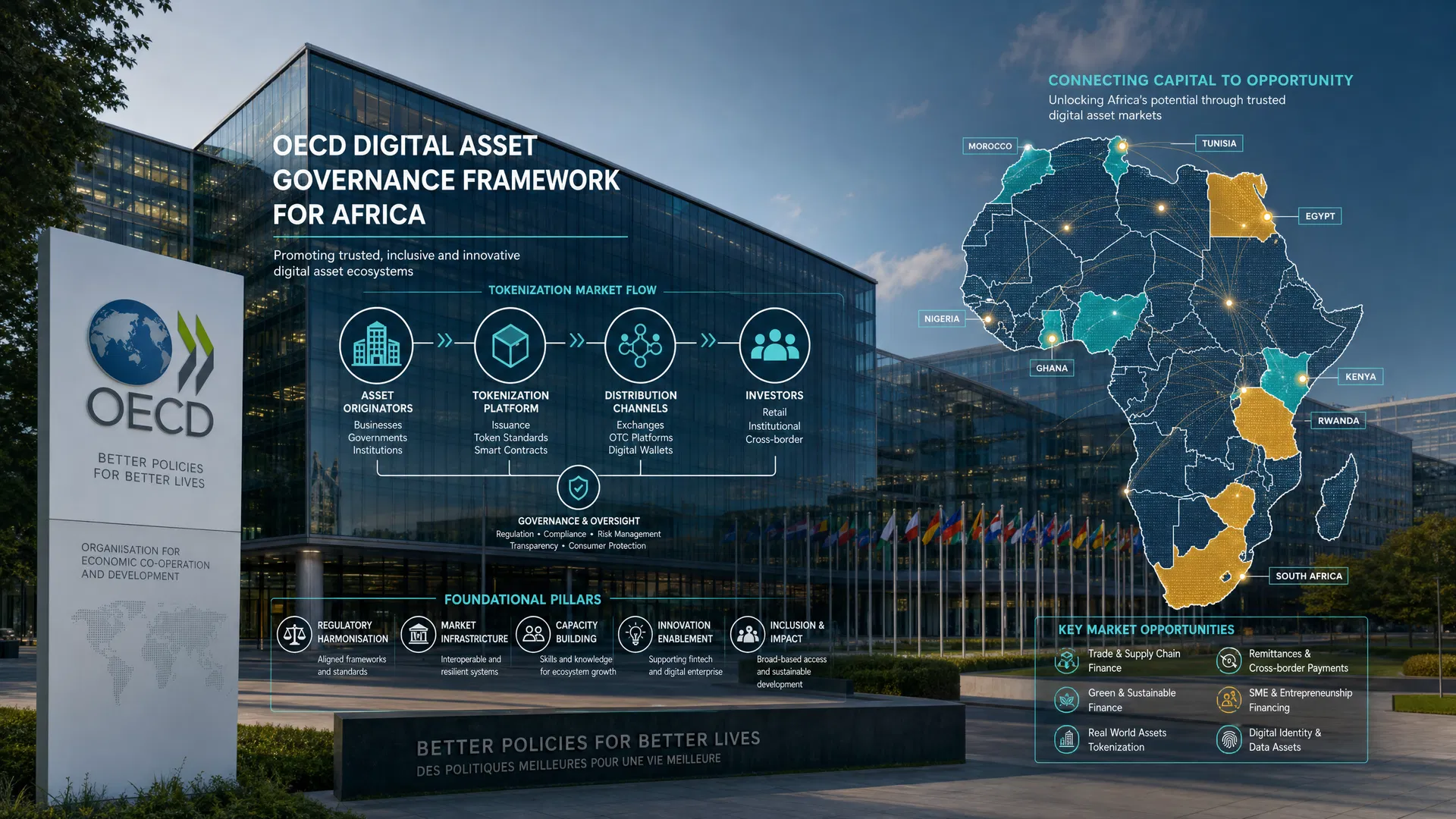

OECD Digital Asset Governance Framework: Implications for African Tokenization Markets

The rapid evolution of digital assets has prompted global regulatory bodies to establish comprehensive governance frameworks, aiming to foster innovation while mitigating systemic risks. The Organisation for Economic Co-operation and Development (OECD) released its Digital Asset Governance Framework in March 2023, providing a structured approach to regulating digital assets including tokenized securities, cryptocurrencies, and stablecoins. For African tokenization markets, which are emerging within a complex milieu of sovereign digital initiatives and evolving regulatory structures, this framework presents both significant opportunities and challenges. This article explores the OECD framework’s regulatory background, key provisions, compliance implications, enforcement mechanisms, and strategic considerations for digital asset platforms in Africa.

Regulatory Background of the OECD Framework

The OECD Framework builds upon a decade of international regulatory collaboration involving the Financial Action Task Force (FATF), the International Organization of Securities Commissions (IOSCO), the Financial Stability Board (FSB), and the International Monetary Fund (IMF). The impetus for the framework arose from the need to harmonize regulatory approaches to digital assets, which often transcend national jurisdictions and expose markets to risks including money laundering, fraud, market manipulation, and financial instability. Published in March 2023, the OECD’s framework aligns with existing international standards such as FATF’s updated recommendations on virtual assets (June 2019), IOSCO’s principles for crypto-asset trading platforms (March 2021), and the IMF’s CBDC operational guidance (October 2022). It complements the FSB’s work on stablecoin regulation and systemic risk assessment.

The framework is designed to be adaptable, recognizing the heterogeneous nature of digital asset markets, including tokenization of real assets, decentralized finance (DeFi), and emerging central bank digital currencies (CBDCs). For Africa, the regulatory context is compounded by regional data protection laws such as South Africa’s Protection of Personal Information Act (POPIA, 2013, fully effective July 2021), Kenya’s Data Protection Act (2019), Ghana’s Data Protection Act (2012), and the Malabo Convention (2014) on personal data protection in Africa. These laws intersect with digital asset governance, particularly in areas such as digital identity verification, transaction transparency, and cross-border data flows. The African Union’s Digital Transformation Strategy for Africa (2020–2030) further underscores the continent’s commitment to digital financial inclusion and sovereign digital infrastructure.

Key Provisions of the OECD Digital Asset Governance Framework

The OECD framework emphasizes four core pillars: regulatory clarity, risk management, consumer protection, and cross-border cooperation. At its foundation, the framework advocates for the clear classification of digital assets, differentiating among payment tokens, utility tokens, security tokens, and hybrid forms. This taxonomy is critical for determining applicable regulatory regimes, which may include securities laws, payments regulation, and anti-money laundering (AML) requirements.

A central provision mandates robust governance structures for digital asset service providers (DASPs), including exchanges, custodians, and token issuers. These entities must implement comprehensive risk management systems addressing market integrity, cybersecurity, and operational resilience. The framework also stresses transparency through mandatory disclosures related to token economics, governance rights, and underlying asset backing, aligning with IOSCO’s principles for asset-backed tokens.

Consumer and investor protection measures are prioritized, requiring clear communication of risks, dispute resolution mechanisms, and safeguards against conflicts of interest. This is particularly relevant for African markets where retail participation in tokenized assets is increasing rapidly, often without adequate investor education. Cross-border regulatory cooperation is another keystone of the framework. It calls for information-sharing agreements, coordinated supervision, and harmonized compliance standards to prevent regulatory arbitrage and illicit finance. This provision is pertinent to Africa, where regional economic communities like the East African Community (EAC) and Economic Community of West African States (ECOWAS) are seeking integrated digital financial ecosystems.

Compliance Implications for African Tokenization Markets

Implementing the OECD framework in African tokenization markets entails significant compliance challenges and opportunities. For institutional investors, adherence to internationally recognized standards such as ISO 20022 for financial messaging and FATF’s virtual asset guidelines is essential to maintain access to global capital markets and avoid sanctions related to AML breaches. AfriVest’s alignment with regional data protection laws—including the NDPA (Nigeria, 2023), PDPA (Rwanda, 2021), and DPA Zimbabwe (2020)—ensures that digital identity and transaction data management comply with privacy norms, a critical factor given the framework’s emphasis on transparency balanced with data protection.

Token issuers must also navigate securities regulation, often evolving in African jurisdictions; for example, Kenya’s Capital Markets Authority updated its Digital Assets Guidelines in 2022 to regulate token offerings and crypto exchanges. Ghana’s Securities and Exchange Commission similarly issued guidelines in 2023 focusing on digital securities issuance.

Conclusion: Advancing Africa’s Digital Economy through Robust Governance

The OECD Digital Asset Governance Framework represents a pivotal milestone in establishing coherent, internationally aligned regulatory standards for digital assets. For Africa’s tokenization markets, the framework offers a blueprint to harmonize innovation with investor protection, financial stability, and data privacy. As countries across the continent advance sovereign digital infrastructures including CBDCs, stablecoins, and digital identity solutions, adherence to this framework will enhance market integrity and attract institutional capital.

By embedding OECD principles within local regulatory regimes and leveraging regional cooperation mechanisms, African policymakers and fintech operators can accelerate the continent’s digital transformation agenda. This will foster inclusive financial ecosystems, enable sustainable capital formation through tokenization, and position Africa as a competitive player in the global digital economy. The path forward demands concerted efforts to balance technological advancement with regulatory prudence, ensuring that Africa’s digital asset markets contribute meaningfully to economic growth and financial inclusion.