Regulatory Background of Payment Service Providers in Africa

Africa’s financial landscape has transformed considerably over the past decade, prompting regulatory frameworks to adapt to innovative payment services. Payment service providers (PSPs) are central to advancing financial inclusion, enabling cross-border trade, and supporting the growing digital economy. In response, regulatory authorities in several African countries have established licensing regimes to govern PSPs, ensuring consumer protection, financial stability, and compliance with international norms.

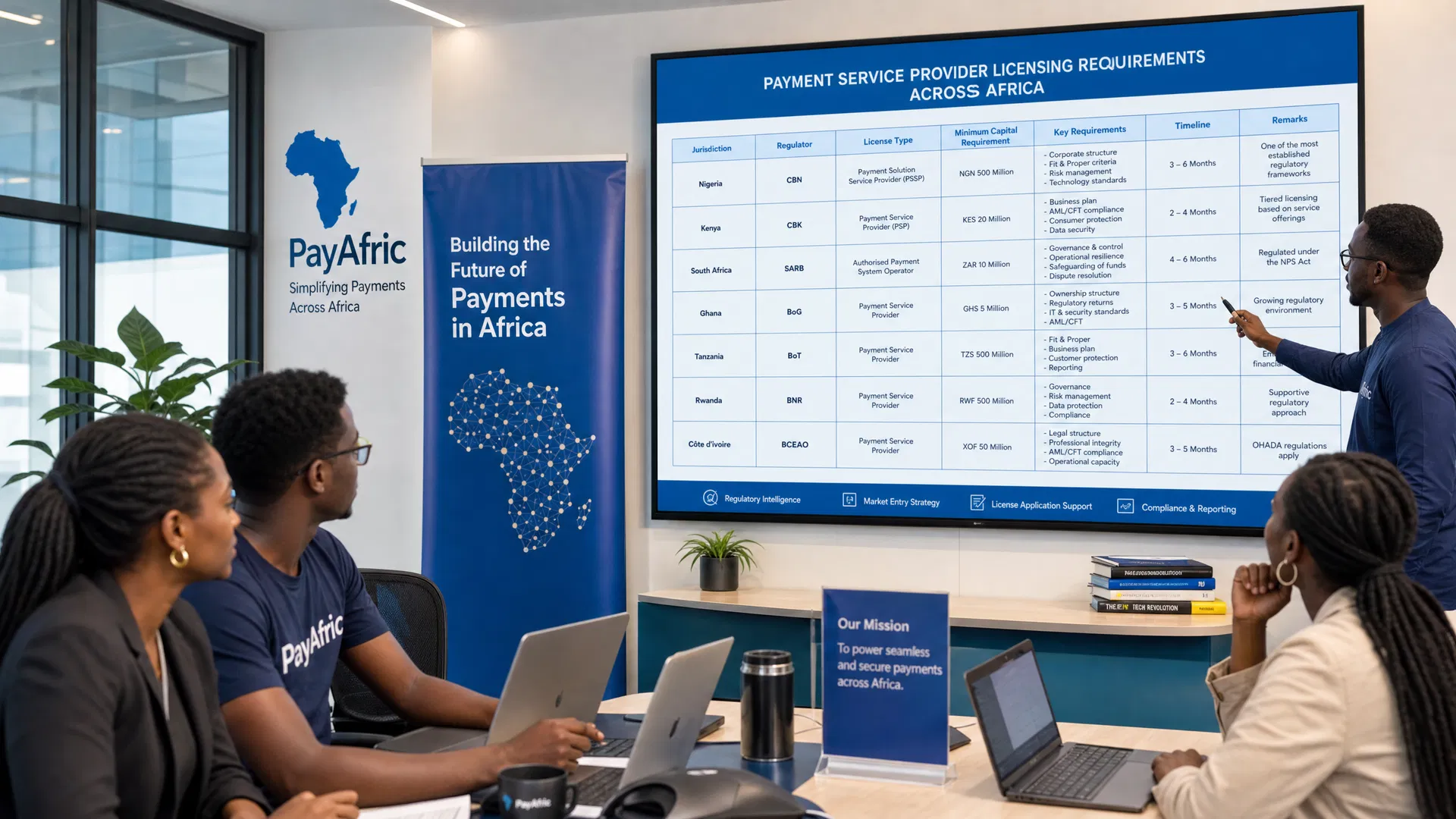

Key frameworks include South Africa’s National Payment System Act (1998), requiring PSP licensure; Nigeria’s Payment Services Banks (PSB) licensing under the Central Bank of Nigeria (CBN) since 2018; Kenya’s Payment Services Act (2019), overseen by the Central Bank of Kenya (CBK); and the West African Economic and Monetary Union (WAEMU) regulations via BCEAO, such as the 2019 electronic money issuance guidelines. These national regulations operate alongside regional policies like the African Continental Free Trade Area (AfCFTA) protocols and the Malabo Convention on Cybersecurity and Personal Data Protection (2014), influencing the cross-border operations of PSPs.

Key Licensing Provisions Across Jurisdictions

Despite variations, African PSP licensing regimes share core provisions aimed at safeguarding the financial system. Entities must demonstrate strong corporate governance, with “fit and proper” criteria for directors and senior managers as enforced by SARB under the National Payment System Act and similarly by the CBN for PSBs.

Capital adequacy requirements ensure operational resilience. For example, Nigeria mandates a minimum capital of ₦2 billion (approx. USD 5 million) for PSBs, while Kenya requires KES 100 million (about USD 900,000) for PSPs. PSPs must implement comprehensive risk management frameworks focused on fraud prevention, cybersecurity, and operational durability, aligning with FATF recommendations and ISO 20022 messaging standards.

Compliance with Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) laws is obligatory. This includes customer due diligence and suspicious transaction reporting, exemplified by Kenya’s Proceeds of Crime and Anti-Money Laundering Act (2019) and South Africa’s Financial Intelligence Centre Act (FICA). PSPs must also prove technical and operational capacity, including settlement processes, safeguarding client funds, and ensuring interoperability, especially given the convergence of digital wallets and mobile money services.

Additionally, jurisdictions demand sound IT infrastructure and data protection compliance under laws such as Ghana’s Data Protection Act (2012), South Africa’s Protection of Personal Information Act (POPIA, 2013), and Kenya’s Data Protection Act (2019), alongside adherence to international technical standards.

Compliance Implications for PSPs

Compliance in African financial markets involves prudential, operational, and legal requirements. PSPs should prioritize governance structures that meet regulators’ expectations for risk management and internal controls. The overlapping jurisdictional demands require integrated compliance programs addressing both financial regulation and data protection.

In East Africa, PSPs must coordinate compliance with both the CBK and Kenya’s Data Protection Commissioner. Cross-border players face harmonization efforts driven by platforms like Financial Sector Deepening (FSD) Africa and the East African Community’s regulatory alignment projects.

Adherence to international AML/CFT frameworks, notably FATF’s 40 Recommendations, is essential to curtail illicit financial flows. Regulators have intensified scrutiny post-2020 to combat rising digital fraud and cybercrime, compelling PSPs to deploy strong customer identification and robust transaction monitoring.

Furthermore, emerging regulations on digital assets—including stablecoins, tokenized assets, and central bank digital currencies (CBDCs)—require vigilant monitoring of regulatory developments aligned with IOSCO principles and IMF CBDC frameworks. These evolving rules affect licensing scopes, operational parameters, and reporting requirements for PSPs associated with digital asset infrastructures.

Enforcement Mechanisms and Regulatory Oversight

Regulatory authorities across Africa wield enforcement powers to ensure PSPs meet licensing conditions and maintain the payment system’s integrity. Enforcement tools include on-site inspections, routine reporting, and sanctions such as fines, license suspension, or revocation.

For instance, the CBN routinely audits PSBs to confirm capital adequacy and imposes penalties for AML breaches. South Africa’s SARB conducts supervisory actions under the National Payment System Act, initiating corrective measures when non-compliance arises.

To bolster oversight, regulators have adopted digital supervisory technologies employing data analytics for real-time transaction monitoring. This enhances transparency and enables prompt detection of irregularities. Regional bodies like the Committee of African Banking Supervisors (CABS) facilitate information exchange and enforcement harmonization, elevating overall regulatory effectiveness.

Preparing Digital Asset Platforms for Regulatory Compliance

Digital asset platforms—engaging in tokenization, stablecoins, and CBDC interactions—must rigorously align with PSP licensing regulations to operate successfully in African markets. This begins with thorough regulatory impact assessments that identify specific jurisdictional requirements and cross-border regulatory considerations.

Platforms should implement advanced compliance frameworks integrating Know Your Customer (KYC), AML, Combating the Financing of Terrorism (CFT), and data protection measures as foundational elements. Adhering to interoperability standards, such as ISO 20022 messaging, enables seamless integration with legacy financial systems and regional payment infrastructures.

Proactive engagement with policymakers and regulators is critical for anticipating regulatory changes and contributing to policy formation, especially amid the fast evolution of digital asset regulations shaped by international entities like the Financial Stability Board (FSB) and OECD.

Managing operational risks via resilient IT architectures and robust incident response plans ensures compliance with data protection laws, exemplified by South Africa’s POPIA and Kenya’s Data Protection Act. Regular audits and continuous compliance training promote a culture conducive to licensing approvals and ongoing regulatory adherence.

Conclusion: Towards a Harmonized Digital Payments Ecosystem in Africa

PSP licensing regimes across African countries embody efforts to balance innovation, financial stability, and consumer protection amid the continent’s dynamic digital economy. For stakeholders like AfriVest, developing sovereign digital asset infrastructure, compliance with these frameworks is essential for institutional investors, policymakers, and fintech operators aiming to leverage Africa’s vast market.

Regional harmonization initiatives under AfCFTA coupled with enhanced cooperation among central banks and data protection authorities are progressively shaping a cohesive regulatory environment. This will enable scalable, interoperable payment solutions incorporating digital assets while supporting financial inclusion.

By actively engaging with licensing requirements and harmonizing operations with international and regional standards, digital asset platforms can unlock Africa’s digital economy potential. This approach fosters trust and stability while catalyzing innovation and sustainable growth throughout the continent’s financial services sector.