# Open Banking Regulations Emerging Across African Financial Markets

The African financial landscape is undergoing a profound transformation, driven by the rapid adoption of digital technologies and the pressing need for financial inclusion. At the heart of this evolution is the emergence of open banking—a framework that mandates or encourages financial institutions to share customer data securely with authorized third-party providers via Application Programming Interfaces (APIs). For AfriVest, as a platform building Africa's sovereign digital asset infrastructure, understanding the nuances of these emerging regulatory frameworks is critical. This article explores the regulatory background, key provisions, compliance implications, and enforcement mechanisms of open banking across African markets, offering insights into how digital asset platforms should prepare for this paradigm shift.

Regulatory Background: A Fragmented Yet Converging Landscape

Unlike the European Union, which implemented a unified approach through the Revised Payment Services Directive (PSD2), Africa's approach to open banking is characterized by a patchwork of national regulations and guidelines. However, a clear trend toward convergence is emerging, driven by the shared goals of fostering innovation, enhancing competition, and expanding financial access.

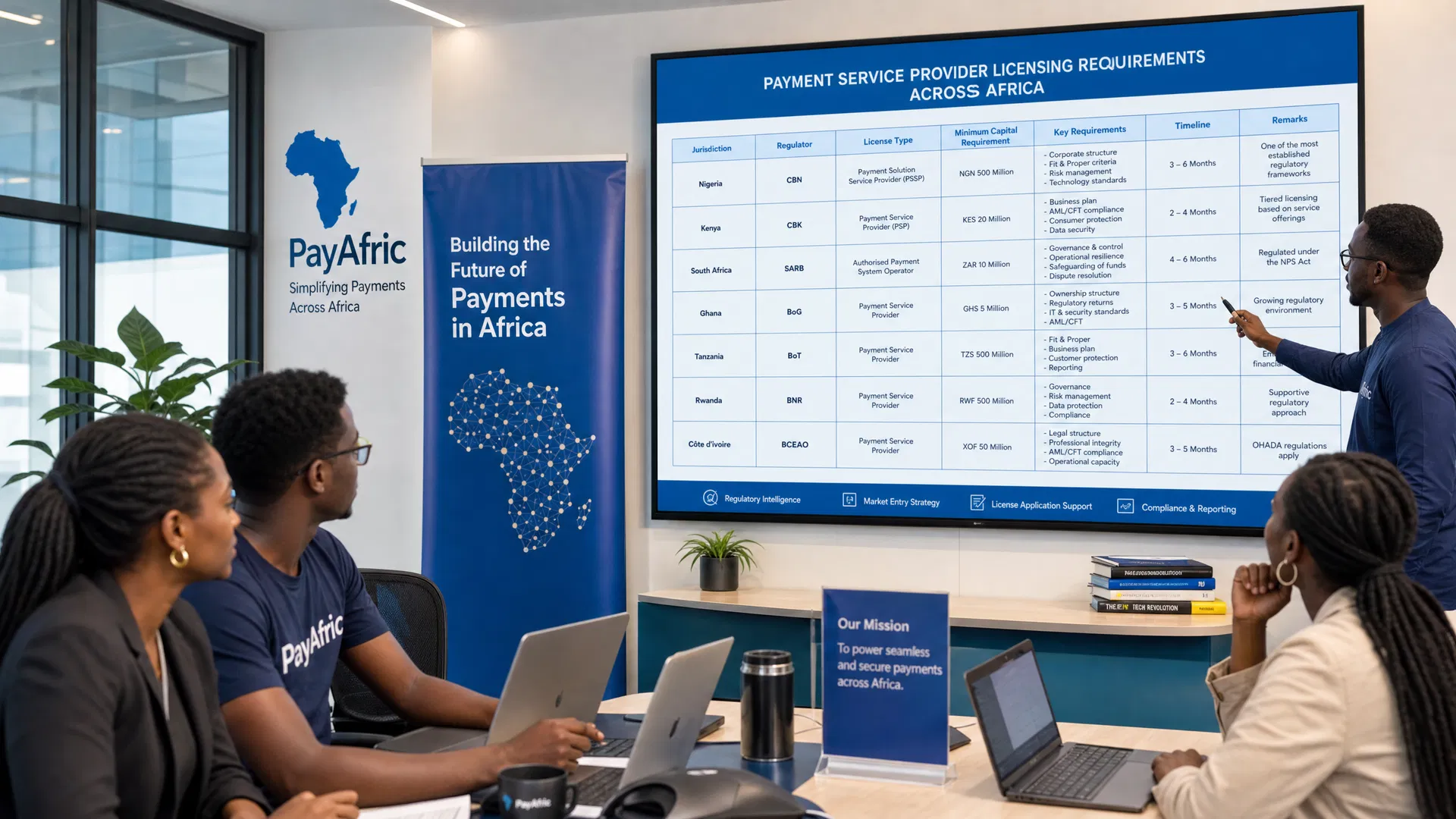

Nigeria has been a trailblazer in this regard. The Central Bank of Nigeria (CBN) issued the Regulatory Framework for Open Banking in Nigeria in 2021, followed by the Operational Guidelines for Open Banking in 2023. These frameworks establish a comprehensive structure for data sharing, categorizing data into different risk tiers and setting stringent requirements for API standards and security.

In East Africa, Kenya is making significant strides. While a formal open banking regulation is still in development, the Central Bank of Kenya (CBK) has actively promoted API standards and data portability as part of its broader National Payments Strategy 2022-2025. The focus here is on leveraging Kenya's robust mobile money ecosystem to create a more interconnected financial environment.

South Africa, possessing one of the continent's most sophisticated financial sectors, is taking a consultative approach. The South African Reserve Bank (SARB) and the Financial Sector Conduct Authority (FSCA) have published consultation papers on open finance, indicating a move toward a formal regulatory framework that balances innovation with risk management.

Key Provisions: Data Protection and API Standardization

The core of any open banking framework lies in its provisions regarding data protection, consent management, and technical standards. Across African jurisdictions, these elements are heavily influenced by regional and international data protection laws.

Consent Management: Explicit, informed, and revocable customer consent is the bedrock of open banking. Regulations require that customers have granular control over what data is shared, with whom, and for how long. This aligns closely with the principles outlined in the Protection of Personal Information Act (POPIA) in South Africa, the Nigeria Data Protection Act (NDPA), and the Data Protection Act (DPA) of Kenya.

Data Protection and Privacy: Open banking frameworks mandate robust data protection measures. Financial institutions and third-party providers must comply with national data protection laws, ensuring data minimization, purpose limitation, and secure storage. The Malabo Convention provides a regional baseline, encouraging harmonization of these standards across the continent.

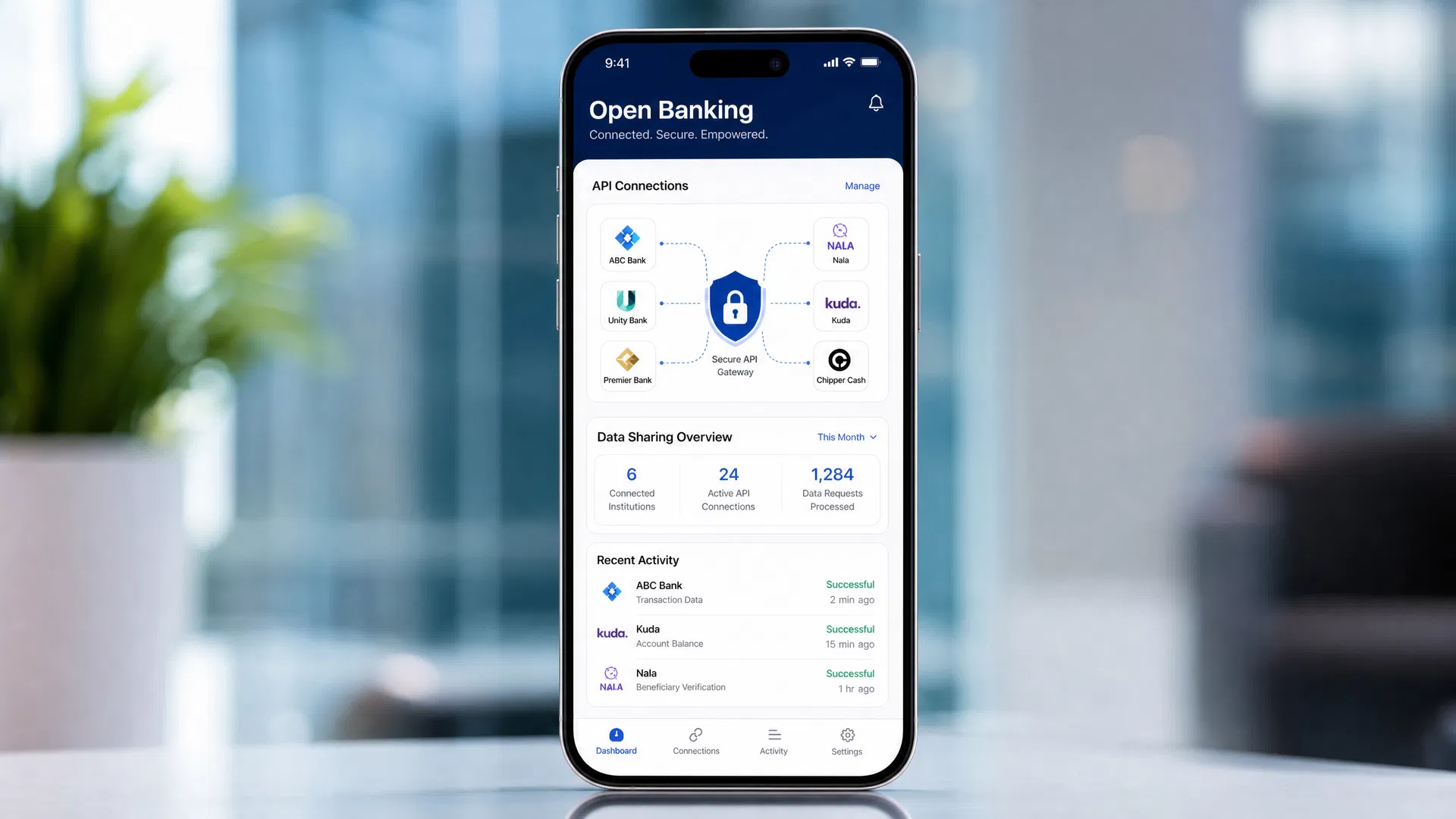

API Standardization: To ensure interoperability and security, regulators are increasingly prescribing specific API standards. The CBN's guidelines, for instance, mandate adherence to international standards such as ISO 20022 for financial messaging. This standardization is crucial for platforms like AfriVest, which operate across multiple jurisdictions and require seamless integration with various financial institutions.

Compliance Implications for Digital Asset Platforms

For digital asset platforms and fintech operators, the emergence of open banking regulations presents both significant opportunities and complex compliance challenges.

Enhanced KYC and AML/CFT: Open banking facilitates access to a wealth of customer financial data, which can significantly enhance Know Your Customer (KYC) and Anti-Money Laundering/Combating the Financing of Terrorism (AML/CFT) processes. By integrating with banks via APIs, platforms can verify identities and assess risk more accurately and efficiently, aligning with Financial Action Task Force (FATF) recommendations.

Data Security and Infrastructure: Compliance requires substantial investment in secure infrastructure. Platforms must implement robust cybersecurity measures, including end-to-end encryption, multi-factor authentication, and continuous monitoring, to protect sensitive financial data. This is particularly relevant for platforms handling digital assets, where security breaches can have severe consequences.

Cross-Border Operations: Navigating the fragmented regulatory landscape is a major challenge for platforms operating across multiple African countries. Compliance teams must stay abreast of evolving regulations in each jurisdiction, ensuring that data sharing practices comply with local laws such as the DPA in Ghana, PDPA in Rwanda, and DPA in Uganda.

Enforcement Mechanisms and Regulatory Oversight

Regulatory bodies across Africa are establishing stringent enforcement mechanisms to ensure compliance with open banking frameworks and data protection laws.

Licensing and Registration: Third-party providers must typically obtain specific licenses or register with the central bank or financial regulator before accessing customer data. The CBN, for example, requires participants to be listed in its Open Banking Registry.

Audits and Reporting: Regulators mandate regular security audits and compliance reporting. Platforms must demonstrate adherence to API standards, data protection protocols, and consent management procedures. Failure to comply can result in severe penalties, including fines, suspension of licenses, or criminal prosecution.

Conclusion: Empowering Africa's Digital Economy

The emergence of open banking regulations across African financial markets is a pivotal development that will significantly accelerate the continent's digital economy transformation. By fostering a secure and standardized environment for data sharing, these frameworks will unlock new opportunities for innovation, enhance financial inclusion, and drive economic growth. For platforms like AfriVest, which are building the infrastructure for Africa's sovereign digital assets, embracing open banking is not just a compliance requirement but a strategic imperative. By aligning with these evolving regulations and prioritizing data protection, digital asset platforms can play a leading role in shaping a more inclusive, efficient, and interconnected financial future for Africa.