# Anti-Money Laundering Regulations Across Sub-Saharan Africa: A Comparative Analysis

As Africa accelerates its digital economy transformation, particularly in the realm of digital assets and financial technology, robust Anti-Money Laundering (AML) frameworks have become paramount. Sub-Saharan Africa, with its diverse regulatory landscape, presents both opportunities and challenges for institutional investors, policymakers, and fintech operators. This article provides a comparative analysis of AML regulations across key Sub-Saharan African jurisdictions, highlighting regulatory backgrounds, key provisions, compliance implications, and enforcement mechanisms. It concludes with strategic considerations for digital asset platforms navigating this evolving environment.

Regulatory Background: International Standards and Regional Adaptations

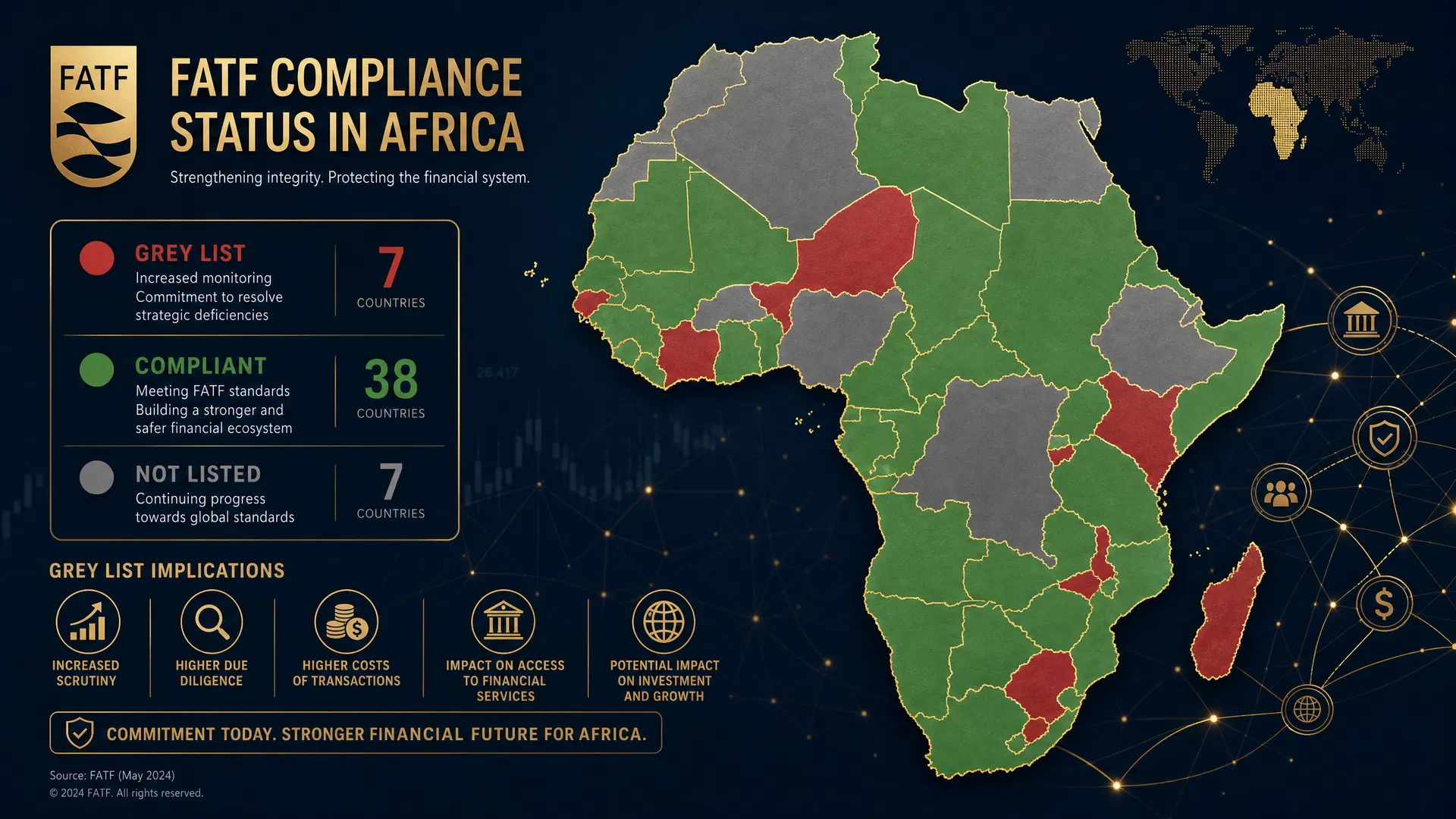

AML regulation in Sub-Saharan Africa is shaped by a combination of international directives and regional legal instruments. The Financial Action Task Force (FATF), established in 1989, remains the global standard-setter, issuing recommendations that emphasize risk-based approaches, customer due diligence (CDD), and beneficial ownership transparency. Most African countries have committed to FATF standards, either directly or through regional bodies such as the Eastern and Southern Africa Anti-Money Laundering Group (ESAAMLG) and the Inter-Governmental Action Group against Money Laundering in West Africa (GIABA).

At the national level, AML laws vary but generally reflect FATF principles. For example, South Africa’s Financial Intelligence Centre Act (FICA) of 2001, amended in 2019, provides a comprehensive framework covering reporting entities, suspicious transaction reporting, and enhanced CDD. Nigeria’s Money Laundering (Prohibition) Act of 2011, amended in 2019, similarly mandates registration of reporting entities and introduces provisions for politically exposed persons (PEPs).

Notably, regional data protection laws, such as South Africa’s Protection of Personal Information Act (POPIA, 2013), Kenya’s Data Protection Act (2019), and the Malabo Convention on Cyber Security and Personal Data Protection (2014), intersect with AML compliance, especially where digital identity and data sharing are concerned. These frameworks require AML programs to incorporate data privacy safeguards, adding complexity to compliance regimes.

Key Provisions Across Jurisdictions

Across Sub-Saharan Africa, AML regimes share several core provisions:

- Customer Due Diligence (CDD) and Know Your Customer (KYC): Mandatory identity verification procedures are required before establishing business relationships. South Africa’s FICA stipulates tiered CDD measures, including simplified due diligence for low-risk customers and enhanced due diligence for high-risk categories.

- Suspicious Transaction Reporting: Reporting entities must submit suspicious transaction reports (STRs) to financial intelligence units (FIUs). Kenya’s Financial Reporting Centre Act (2018) established the Financial Reporting Centre (FRC) as the central FIU, requiring timely STR submissions.

- Beneficial Ownership Transparency: Nigeria’s AML regulations require disclosure of ultimate beneficial owners to prevent misuse of corporate structures. Ghana’s Anti-Money Laundering Act, 2020 also mandates similar transparency.

- Politically Exposed Persons (PEPs) Identification: Enhanced monitoring of PEPs is standard to mitigate corruption risks. Uganda’s Anti-Money Laundering Act (2013) includes detailed provisions on PEPs.

- Record Keeping: Institutions must retain transaction records for a minimum period, typically five years, as seen in Zimbabwe’s Money Laundering and Proceeds of Crime Act (2017).

- Risk-Based Approach: Most jurisdictions require institutions to implement risk assessments and tailor AML controls accordingly. ESAAMLG’s mutual evaluations promote this principle.

Compliance Implications for Digital Asset Platforms

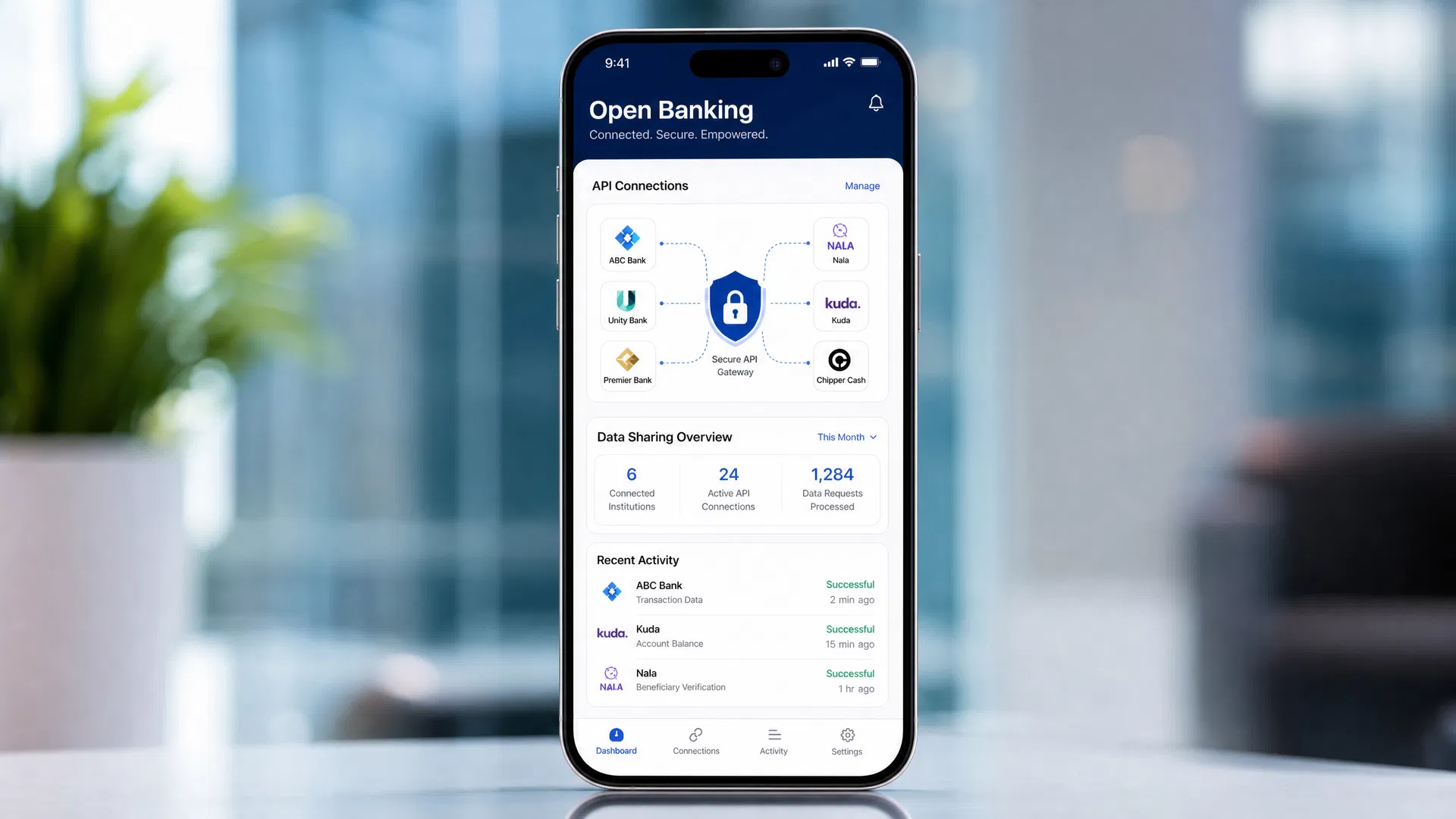

Digital asset platforms operating in Sub-Saharan Africa must navigate these AML requirements while integrating emerging technologies such as tokenization, Central Bank Digital Currency (CBDC) infrastructure, and digital identity solutions. The decentralized and pseudonymous nature of many digital assets presents unique challenges to traditional AML compliance frameworks.

Platforms must implement robust KYC processes aligned with national regulator expectations. For instance, South Africa’s Financial Sector Conduct Authority (FSCA) has emphasized that crypto-asset service providers fall under FICA’s ambit, requiring registration and adherence to AML/CFT controls. Nigeria’s Securities and Exchange Commission (SEC) similarly requires digital asset exchanges to comply with AML obligations under the Money Laundering (Prohibition) Act.

Given the increasing adoption of interoperable digital identity systems, compliant platforms should leverage secure, privacy-preserving digital ID solutions that align with regional data protection laws such as POPIA and Kenya’s Data Protection Act. This harmonization facilitates enhanced CDD without compromising user privacy.

Stablecoin issuers and CBDC infrastructure providers face additional scrutiny. The Bank of International Settlements (BIS) and International Monetary Fund (IMF) frameworks encourage integration of AML controls within CBDC design, including transaction monitoring and real-time reporting to FIUs. AfriVest’s alignment with these standards ensures that sovereign digital asset initiatives embed compliance from inception.

Enforcement Mechanisms and Institutional Oversight

Enforcement of AML regulations in Sub-Saharan Africa is primarily vested in FIUs, central banks, and financial sector regulators. The effectiveness of enforcement varies across countries, influenced by institutional capacity, legal frameworks, and political will.

In South Africa, the Financial Intelligence Centre (FIC) is empowered to investigate and sanction non-compliance, with penalties reaching fines of up to ZAR 10 million or imprisonment. Kenya’s FRC has increasingly enforced compliance through administrative actions and public advisories against non-compliant entities. Nigeria’s Economic and Financial Crimes Commission (EFCC), in collaboration with the Nigerian SEC, actively prosecutes money laundering offenses linked to digital assets.

Cross-border cooperation is facilitated through regional bodies such as ESAAMLG and GIABA, which conduct mutual evaluations and foster information sharing. However, challenges remain due to disparities in regulatory sophistication and resource constraints.

Moreover, the integration of digital asset platforms into AML enforcement introduces novel technical requirements. Real-time transaction monitoring, blockchain analytics, and AI-driven anomaly detection are becoming essential tools for regulators and compliance officers alike.

Preparing Digital Asset Platforms for AML Compliance

To operate effectively within Sub-Saharan Africa’s AML regulatory environment, digital asset platforms must adopt a proactive, multi-faceted compliance strategy. Key preparatory steps include:

- Regulatory Mapping and Licensing: Conduct thorough jurisdictional analyses to identify applicable AML laws and obtain necessary licenses or registrations from relevant authorities such as the South African FSCA, Nigerian SEC, or Kenyan FRC.

- Robust KYC and CDD Processes: Deploy digital identity verification systems that comply with national data protection laws and enable tiered due diligence aligned with risk profiles.

- Transaction Monitoring and Reporting: Implement automated systems capable of identifying suspicious activities and generating timely STRs to FIUs, incorporating blockchain analytics where applicable.

- Staff Training and Governance: Establish AML compliance units with trained personnel and clear governance structures to oversee policy implementation and regulatory liaison.

- Data Privacy Integration: Ensure AML programs respect data protection mandates under POPIA, NDPA (Namibia), and similar laws, balancing transparency with privacy rights.

- Engagement with Regulators and Industry Bodies: Maintain active communication with regulators and participate in regional AML forums to stay abreast of evolving standards and enforcement trends.

Conclusion: AML Compliance as a Pillar of Africa’s Digital Economy

As Sub-Saharan Africa embraces digital asset innovation, effective AML regulation and compliance serve as critical enablers of trust and financial integrity. The region’s diverse yet increasingly harmonized AML frameworks, grounded in FATF standards and complemented by regional data protection laws, represent a maturing regulatory ecosystem.

Digital asset platforms that integrate comprehensive AML controls, aligned with international best practices and local statutory requirements, will be well-positioned to contribute to Africa’s digital economy transformation. Sovereign initiatives such as CBDCs, alongside private sector tokenization and fintech solutions, depend on a robust compliance foundation to foster inclusion, mitigate illicit finance risks, and attract institutional investment.

AfriVest’s commitment to aligning Africa’s sovereign digital asset infrastructure with global AML and data protection standards exemplifies the strategic approach necessary to navigate this complex landscape. As regulatory frameworks continue to evolve, ongoing collaboration among policymakers, industry participants, and international bodies will be essential to harness the full potential of digital finance across Sub-Saharan Africa.

---

References:

- Financial Action Task Force (FATF) Recommendations, 2012 (updated 2019)

- South Africa Financial Intelligence Centre Act (FICA), Act No. 38 of 2001, amended 2019

- Nigeria Money Laundering (Prohibition) Act, 2011, amended 2019

- Kenya Financial Reporting Centre Act, 2018

- Ghana Anti-Money Laundering Act, 2020

- Uganda Anti-Money Laundering Act, 2013

- Zimbabwe Money Laundering and Proceeds of Crime Act, 2017

- Protection of Personal Information Act (POPIA), South Africa, 2013

- Kenya Data Protection Act, 2019

- Malabo Convention on Cyber Security and Personal Data Protection, 2014

- Bank of International Settlements (BIS) – Central Bank Digital Currency frameworks, 2020

- IMF CBDC Regulatory Guidance, 2021

- ESAAMLG Mutual Evaluation Reports, various years