Navigating FATF Compliance in Africa: Grey List Implications and National Remediation Strategies

The global regulatory landscape for digital assets is evolving rapidly, and Africa is at the forefront of this transformation. As the continent embraces digital innovation, the intersection of financial inclusion and regulatory compliance has become a critical focal point. For institutional investors, policymakers, and fintech operators, understanding the implications of the Financial Action Task Force (FATF) standards is paramount. The FATF's role in combating money laundering and terrorist financing (AML/CFT) shapes the operational environment for digital asset platforms, particularly concerning the "grey list" and the subsequent national remediation strategies adopted by African nations.

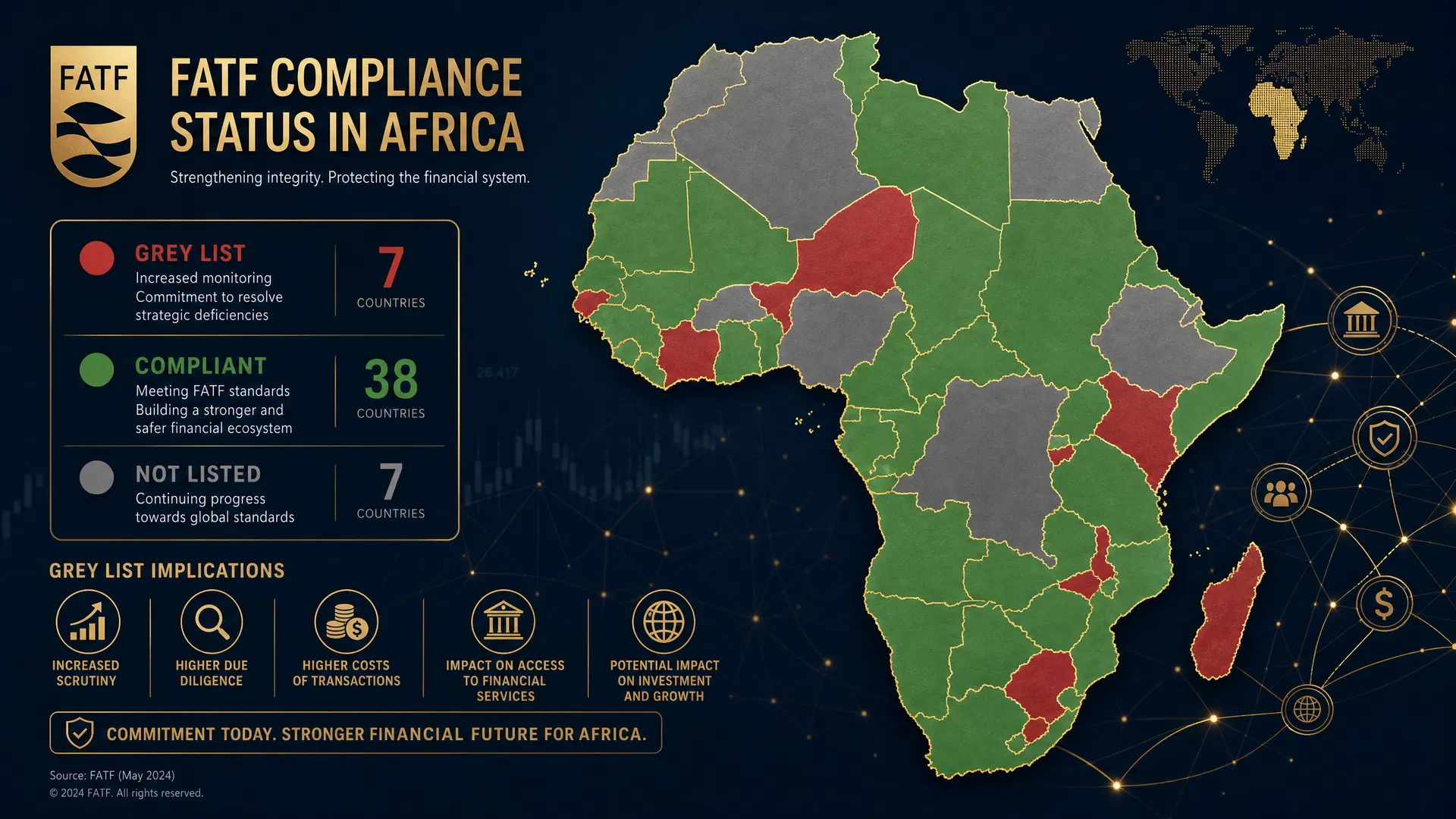

The FATF, a Paris-based intergovernmental organization, sets international standards to prevent financial crimes. Jurisdictions under increased monitoring, commonly referred to as being on the "grey list," are actively working with the FATF to address strategic deficiencies in their AML/CFT regimes. In recent years, several African countries, including economic powerhouses like South Africa and Nigeria, found themselves on this list. This designation carries significant economic and reputational consequences, potentially deterring foreign investment and increasing administrative burdens for cross-border transactions. However, it also serves as a catalyst for comprehensive regulatory reform, driving nations to align their financial systems with global standards.

The Economic Impact of Grey Listing on African Markets

Being placed on the FATF grey list can have profound implications for a country's economy. It signals to the international community that a jurisdiction has structural weaknesses in its financial regulatory framework. For Africa, a continent heavily reliant on foreign direct investment and international trade, this can lead to increased scrutiny from global financial institutions. Banks may implement enhanced due diligence measures, leading to delays in cross-border payments and higher compliance costs. This environment poses unique challenges for digital asset platforms, which rely on seamless international transactions and robust banking relationships to operate effectively.

Despite these challenges, the grey listing process often accelerates necessary regulatory advancements. For instance, following their inclusion on the list in early 2023, both South Africa and Nigeria embarked on aggressive remediation strategies. These efforts involved updating legislative frameworks, enhancing the capabilities of financial intelligence units, and implementing stricter oversight mechanisms. The recent removal of South Africa, Nigeria, Mozambique, and Burkina Faso from the grey list in October 2025 underscores the effectiveness of these national remediation strategies and highlights the continent's commitment to financial integrity.

Key Provisions and Compliance Implications for Digital Assets

The FATF Recommendations provide a comprehensive framework that countries must implement to combat financial crimes. For the digital asset sector, Recommendation 15 is particularly relevant, as it addresses new technologies and virtual asset service providers (VASPs). This recommendation requires jurisdictions to assess and mitigate the risks associated with virtual assets and to ensure that VASPs are regulated for AML/CFT purposes. Compliance implies implementing robust Know Your Customer (KYC) procedures, transaction monitoring, and adhering to the "Travel Rule," which mandates the sharing of originator and beneficiary information during virtual asset transfers.

For platforms like AfriVest, which is building Africa's sovereign digital asset infrastructure, aligning with these provisions is not merely a regulatory requirement but a strategic imperative. AfriVest's integration of international standards, including ISO 20022, IOSCO, and IMF CBDC frameworks, positions it as a compliant and secure platform. Furthermore, adherence to regional data protection laws, such as South Africa's POPIA, Nigeria's NDPA, and the Malabo Convention, ensures that AML/CFT measures do not compromise user privacy. This dual focus on security and privacy is essential for building trust among institutional investors and the broader public.

Enforcement Mechanisms and Institutional Oversight

The enforcement of FATF standards relies heavily on national regulatory bodies and financial intelligence units. In Africa, institutions such as the Financial Intelligence Centre (FIC) in South Africa and the Economic and Financial Crimes Commission (EFCC) in Nigeria play pivotal roles in monitoring compliance and investigating financial crimes. These bodies are empowered to conduct audits, impose sanctions, and collaborate with international counterparts to track illicit financial flows. The effectiveness of these enforcement mechanisms is a critical component of the FATF's mutual evaluation process, which assesses a country's compliance with the standards.

Digital asset platforms must proactively engage with these regulatory bodies to ensure ongoing compliance. This involves regular reporting, participating in industry consultations, and demonstrating a commitment to transparency. By fostering a collaborative relationship with regulators, platforms can help shape a regulatory environment that supports innovation while mitigating risks. AfriVest's approach, which emphasizes alignment with both global standards and regional frameworks, exemplifies how digital asset infrastructure can operate harmoniously within a stringent regulatory landscape.

Preparing for the Future: Strategies for Digital Asset Platforms

As African nations continue to strengthen their AML/CFT regimes, digital asset platforms must adopt forward-looking strategies to navigate the evolving regulatory environment. This requires a proactive approach to compliance, integrating advanced technologies such as artificial intelligence and blockchain analytics to enhance transaction monitoring and risk assessment. Platforms must also invest in continuous training for their compliance teams to stay abreast of regulatory changes and emerging typologies of financial crime.

Furthermore, platforms should actively participate in regional harmonization efforts. Initiatives aimed at creating cohesive regulatory frameworks across the continent, such as those supported by the African Continental Free Trade Area (AfCFTA), present opportunities to streamline compliance processes and facilitate cross-border operations. By aligning their operations with these regional initiatives, digital asset platforms can contribute to the broader goal of financial integration in Africa.

Conclusion: Driving Africa's Digital Economy Transformation

The journey toward FATF compliance and the successful execution of national remediation strategies represent a critical phase in Africa's economic development. While the challenges associated with grey listing are significant, they also provide an impetus for building more resilient and transparent financial systems. For digital asset platforms, navigating this landscape requires a steadfast commitment to compliance, innovation, and collaboration with regulatory authorities.

As Africa continues its digital economy transformation, platforms like AfriVest are uniquely positioned to lead the way. By building infrastructure that aligns with international standards and regional data protection laws, AfriVest not only ensures regulatory compliance but also fosters financial inclusion and economic growth. The successful integration of digital assets into Africa's financial ecosystem will ultimately depend on the ability of stakeholders to balance innovation with the imperative of financial integrity, paving the way for a secure and prosperous digital future.