The Evolution of Know Your Customer Frameworks in African Digital Finance

The rapid expansion of digital finance across the African continent has necessitated a fundamental reevaluation of regulatory frameworks governing customer identification and verification. As mobile money platforms, digital asset exchanges, and decentralized finance protocols proliferate, regulatory authorities are increasingly focused on mitigating risks associated with money laundering, terrorist financing, and illicit financial flows. Know Your Customer (KYC) requirements serve as the foundational pillar of these regulatory efforts, establishing the mechanisms through which financial institutions and digital asset service providers verify the identities of their clientele. The implementation of robust KYC standards is not merely a compliance exercise but a critical prerequisite for integrating African financial systems into the global economy.

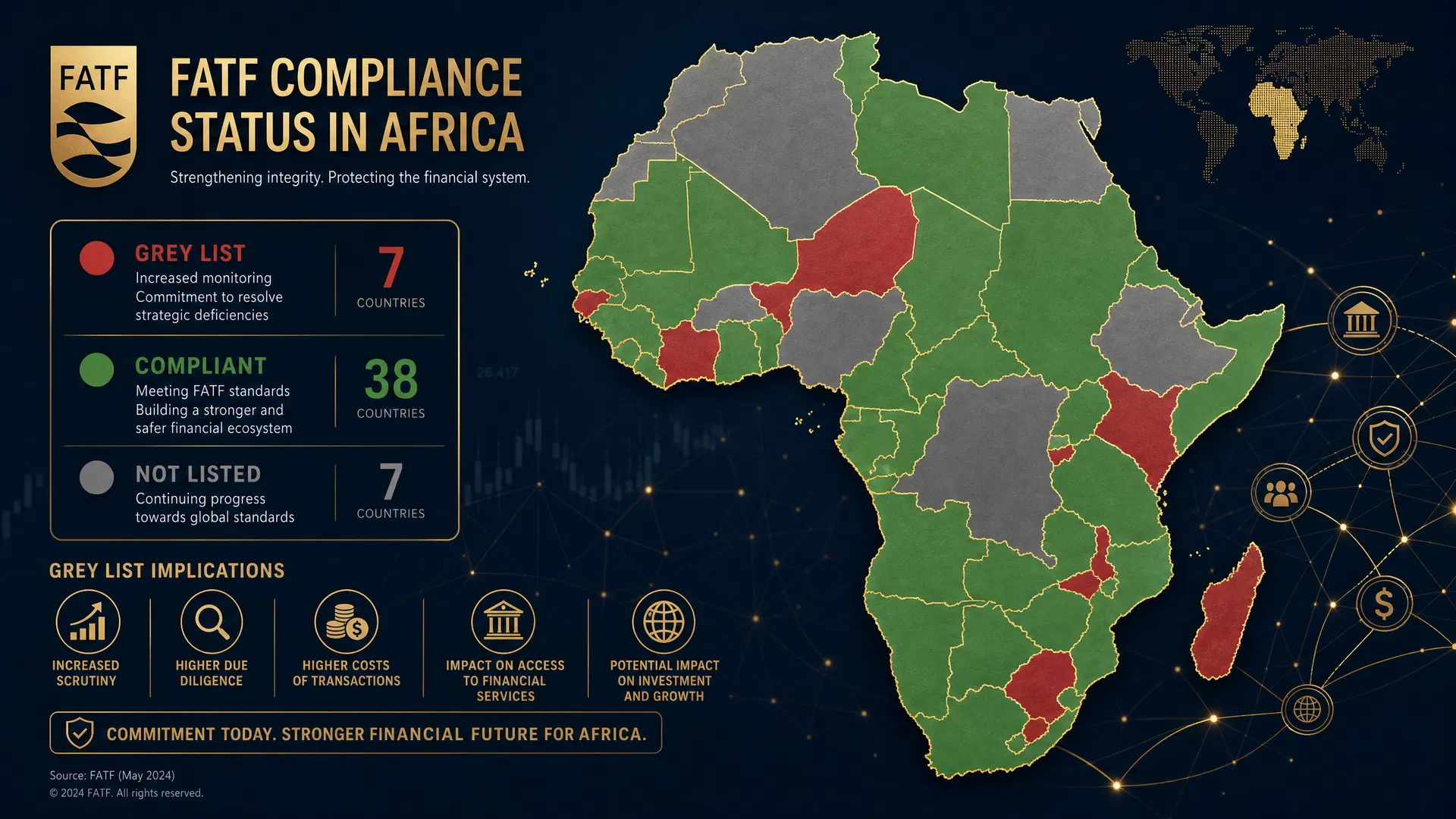

Historically, the reliance on paper-based identification systems and the prevalence of informal economic activities presented significant challenges for KYC compliance in many African jurisdictions. However, the advent of digital identity infrastructure and the harmonization of regional regulatory standards have catalyzed a paradigm shift. Organizations such as the Financial Action Task Force (FATF) have provided comprehensive guidelines that African nations are increasingly adopting and adapting to their unique socioeconomic contexts. This regulatory evolution is particularly pertinent for platforms like AfriVest, which are building sovereign digital asset infrastructure aligned with international standards such as ISO 20022 and the frameworks established by the International Monetary Fund (IMF) and the Financial Stability Board (FSB).

Key Provisions and Legislative Mandates Across Jurisdictions

The regulatory landscape governing KYC in Africa is characterized by a complex interplay of national legislation and regional directives. At the core of these frameworks are stringent requirements for customer due diligence (CDD) and enhanced due diligence (EDD) for high-risk entities. In South Africa, the Financial Intelligence Centre Act (FICA) of 2001, significantly amended in 2017, mandates accountable institutions to establish and verify the identities of their clients, maintain comprehensive records, and report suspicious transactions. The Financial Sector Conduct Authority (FSCA) has further extended these requirements to crypto asset service providers, designating them as accountable institutions effective December 2022.

Similarly, Nigeria's Money Laundering (Prevention and Prohibition) Act of 2022, enforced by the Economic and Financial Crimes Commission (EFCC) and the Central Bank of Nigeria (CBN), imposes rigorous KYC obligations on financial institutions and designated non-financial businesses. The CBN's revised regulatory framework for mobile money services and digital financial operations explicitly requires tiered KYC structures, balancing financial inclusion objectives with anti-money laundering (AML) imperatives. In Kenya, the Proceeds of Crime and Anti-Money Laundering Act (POCAMLA) of 2009, overseen by the Financial Reporting Centre (FRC), establishes the legal basis for KYC compliance, with recent amendments explicitly capturing digital asset transactions and virtual asset service providers.

Furthermore, the intersection of KYC requirements and data protection laws is increasingly prominent. The processing of sensitive personal data for identity verification must comply with regional and national data privacy frameworks. The Malabo Convention on Cyber Security and Personal Data Protection, alongside national laws such as South Africa's Protection of Personal Information Act (POPIA) of 2013, Nigeria's Data Protection Act (NDPA) of 2023, and Kenya's Data Protection Act of 2019, mandate strict safeguards for the collection, storage, and processing of KYC data. Financial institutions must navigate the dual imperatives of comprehensive identity verification and stringent data privacy compliance.

Compliance Implications for Digital Asset Platforms

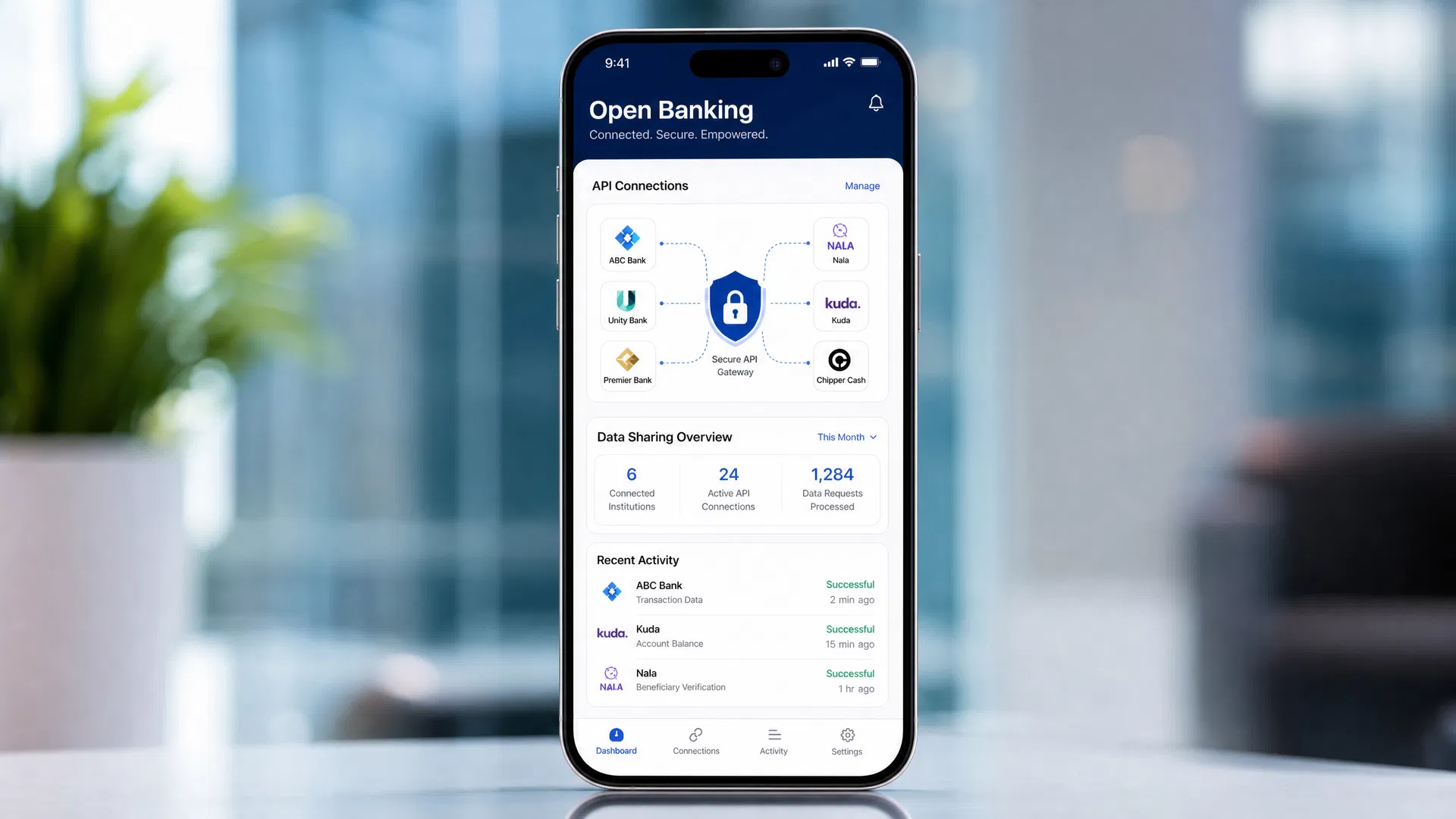

For digital asset platforms and fintech operators, the implementation of KYC requirements necessitates sophisticated technological infrastructure and robust operational protocols. Consequently, platforms must deploy advanced identity verification solutions, leveraging biometric authentication, artificial intelligence, and machine learning algorithms to detect fraudulent documentation and assess risk profiles in real-time.

Moreover, the decentralized nature of certain digital assets introduces unique compliance challenges. The FATF's Recommendation 15, which addresses new technologies and virtual assets, requires jurisdictions to regulate virtual asset service providers (VASPs) for AML and counter-terrorist financing (CFT) purposes. This includes the implementation of the "Travel Rule," which mandates the collection and transmission of originator and beneficiary information during digital asset transfers. For platforms operating across multiple African jurisdictions, achieving compliance with the Travel Rule requires interoperable systems and standardized data formats, such as ISO 20022, to facilitate secure information exchange between institutions.

Enforcement Mechanisms and Regulatory Oversight

Regulatory authorities across the African continent are adopting increasingly assertive enforcement postures to ensure compliance with KYC and AML mandates. The mechanisms of enforcement range from routine supervisory inspections and thematic reviews to the imposition of substantial administrative sanctions and criminal prosecutions.

In jurisdictions such as Nigeria and South Africa, regulatory bodies have demonstrated a willingness to levy significant financial penalties on institutions that fail to implement adequate KYC controls. The South African Reserve Bank (SARB) and the FSCA have issued substantial fines and directives for remedial action against entities exhibiting systemic deficiencies in their AML/CFT frameworks.

Conclusion: Securing Africa's Digital Economy Transformation

The rigorous implementation of Know Your Customer requirements is not an impediment to innovation but a fundamental enabler of Africa's digital economy transformation. As the continent transitions toward sovereign digital asset infrastructure, encompassing tokenization, central bank digital currencies (CBDCs), and decentralized financial services, the integrity of the financial system remains paramount.

For platforms like AfriVest, the strategic integration of advanced identity verification technologies and comprehensive compliance protocols is essential for building resilient and scalable digital financial ecosystems. By prioritizing regulatory compliance and fostering transparent, secure financial environments, African digital asset platforms can mitigate systemic risks and position the continent as a formidable participant in the global digital economy.