The Imperative for Digital Currency Harmonization in Pan-Africa

Africa's digital economy is undergoing a transformative shift, driven by rapid mobile penetration, fintech innovation, and increasing interest in blockchain technologies. Central to this evolution is the emergence of digital currencies, particularly central bank digital currencies (CBDCs), which offer the potential to streamline payments, enhance financial inclusion, and reduce transaction costs across the continent. However, the fragmented regulatory landscape and diverse monetary policies across African nations present significant challenges to the seamless adoption and interoperability of digital currencies.

Harmonization strategies for digital currency across Pan-Africa are essential to unlock the full benefits of this digital revolution. Currently, over 70% of Sub-Saharan Africa’s population remains underserved by traditional banking systems, while mobile money accounts for over 50% of financial transactions in countries like Kenya and Ghana. This disparity underscores the need for unified frameworks that can accommodate varied economic contexts yet provide a common platform for digital currency issuance, regulation, and cross-border functionality. Without these harmonized strategies, the risk of regulatory arbitrage, currency fragmentation, and slowed adoption of CBDCs will likely persist, hindering continental integration.

Central Bank Digital Currency (CBDC) Initiatives Across Africa

Several African central banks have already embarked on CBDC pilots, signaling a growing commitment to leveraging digital currencies for economic modernization. Nigeria's eNaira, launched in 2021, is among the continent's most prominent CBDC projects, aiming to boost financial inclusion and reduce transaction costs. Similarly, the Central Bank of Ghana has piloted the digital Cedi, targeting improved payment efficiency and enhanced monetary policy implementation. These initiatives reflect a continent-wide trend: using CBDCs not only as a payment tool but also as a means to digitize the financial ecosystem and reinforce regulatory oversight.

Despite these advances, the varying stages of CBDC development underscore the urgency for a harmonized Pan-African approach. For example, while Nigeria experiences over 100 million mobile money accounts, countries like Angola and Zimbabwe are still building foundational digital payment infrastructure. Harmonization strategies would promote interoperability between such diverse systems, enabling smoother cross-border remittances and trade settlements. Furthermore, coordinated regulatory frameworks would mitigate risks related to digital currency fraud, cybersecurity, and money laundering, which remain concerns given the nascent nature of CBDCs in the region.

Blockchain and Tokenization as Catalysts for Digital Currency Integration

Blockchain technology and tokenization present transformative opportunities to complement digital currency harmonization efforts in Pan-Africa. By enabling decentralized, transparent, and secure transactions, blockchain can address many of the inefficiencies inherent in traditional payment systems. Tokenization, the process of converting assets into digital tokens on a blockchain, facilitates liquidity and fractional ownership, which can democratize access to financial markets and assets across borders.

In practice, African fintech startups are already harnessing blockchain for cross-border payments, supply chain finance, and digital identity verification. For instance, BitPesa operates on a blockchain framework to provide faster and cheaper remittance services between African countries and the global market. Tokenization of real assets, such as agricultural commodities or real estate, can also amplify financial inclusion by enabling investors to participate in markets previously inaccessible due to high entry costs. Integrating these technologies with CBDCs and harmonized regulatory frameworks would create a resilient digital currency ecosystem, capable of supporting Africa's rapidly expanding digital economy.

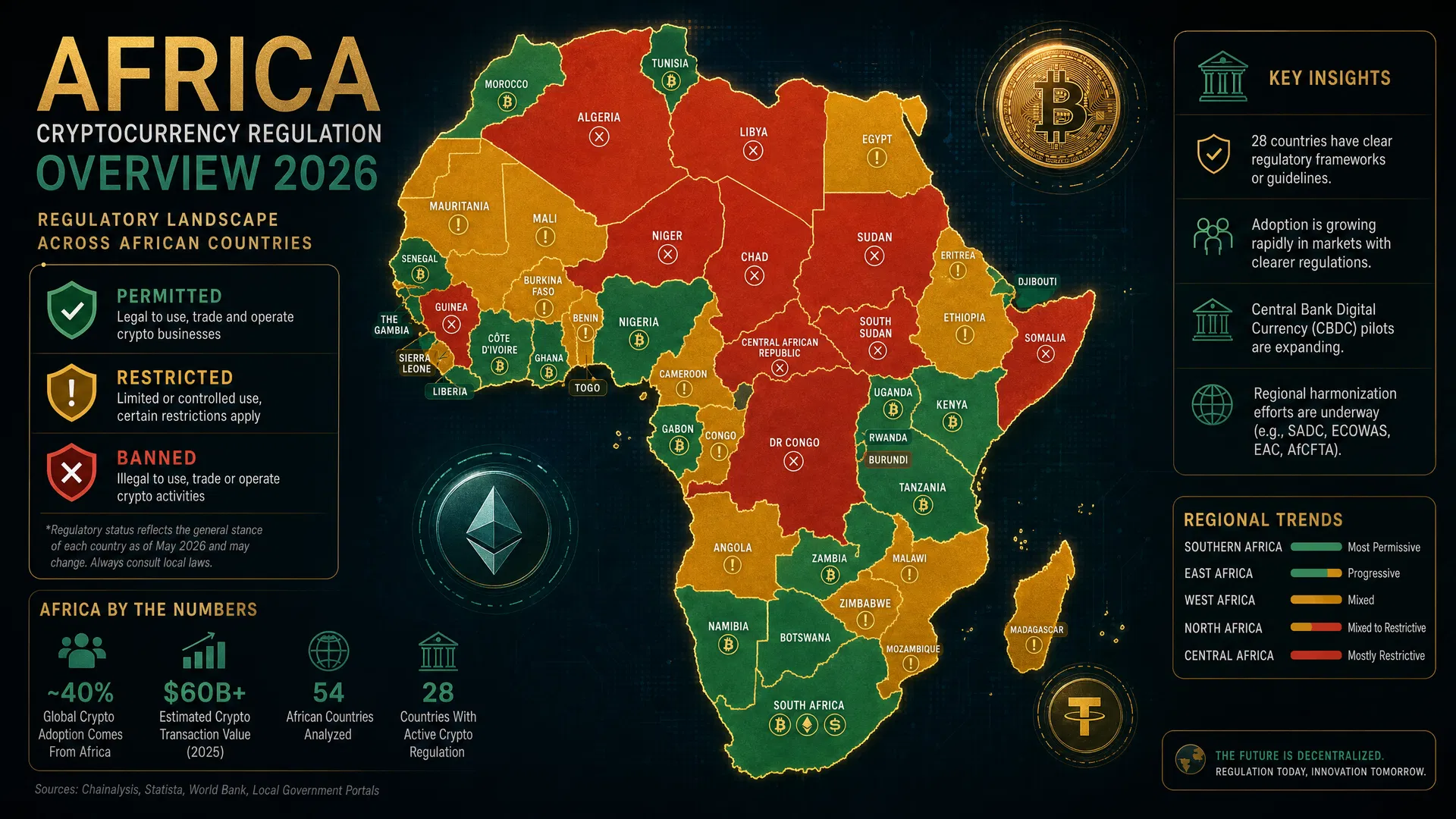

Regulatory Frameworks and the Need for Pan-African Collaboration

A significant barrier to digital currency harmonization in Africa is the heterogeneous regulatory environment. National authorities often adopt disparate approaches to digital currency oversight, reflecting differing levels of technological readiness, economic priorities, and risk tolerance. For instance, while the South African Reserve Bank has taken a cautious, consultative approach to CBDCs, some countries have remained skeptical or imposed strict regulations on cryptocurrencies. This regulatory patchwork complicates the prospect of interoperable digital currencies and cross-border transactions.

To address these challenges, Pan-African institutions such as the African Union and the African Export-Import Bank (Afreximbank) have advocated for regional regulatory harmonization. The African Continental Free Trade Area (AfCFTA) also provides a framework to support cross-border digital payment systems and harmonized financial regulations. Collaborative efforts could standardize compliance requirements, data privacy protocols, and anti-money laundering (AML) measures, thereby fostering investor confidence and facilitating scalable digital currency adoption. Such unified frameworks would also be instrumental in shaping policy discussions around CBDC design, issuance, and integration into existing financial infrastructures.

Economic and Social Impacts of Harmonized Digital Currency Systems

The harmonization of digital currencies across Pan-Africa promises to generate significant economic and social value. Economically, it would reduce transaction costs for businesses and consumers, facilitate faster cross-border trade, and improve the efficiency of monetary policy transmission. For example, cross-border remittances, which account for over $48 billion annually to Sub-Saharan Africa, could see dramatic reductions in fees and processing times through interoperable CBDC networks.

Socially, harmonized digital currencies can accelerate financial inclusion for marginalized populations, particularly women, youth, and rural communities who traditionally lack access to banking services. By integrating with mobile money platforms, CBDCs can leverage existing user bases and digital identities to onboard millions more into the formal financial system. Moreover, transparent and secure digital currency systems can enhance trust in financial institutions and reduce corruption risks. The ripple effects of such inclusion extend to improved access to credit, savings, and insurance products, fostering sustainable economic growth and poverty alleviation.

Looking Ahead: Building a Robust Digital Infrastructure for Pan-African Integration

As Africa embraces the digital currency revolution, the need for robust digital infrastructure and cohesive harmonization strategies becomes paramount. Investments in secure payment rails, blockchain networks, and regulatory technology (RegTech) are critical to supporting scalable and resilient CBDC ecosystems. Public-private partnerships will play a vital role in mobilizing resources and expertise to build interoperable platforms that serve diverse economic contexts across the continent.

Looking forward, digital currency harmonization offers a unique opportunity to propel Pan-Africa towards economic integration and technological leadership. By aligning regulatory frameworks, leveraging blockchain and tokenization innovations, and prioritizing inclusive infrastructure development, African policymakers and institutional investors can unlock unprecedented growth in the continent’s digital economy. The path forward demands visionary collaboration, continuous innovation, and a commitment to harnessing digital currencies as a catalyst for sustainable development and regional prosperity.