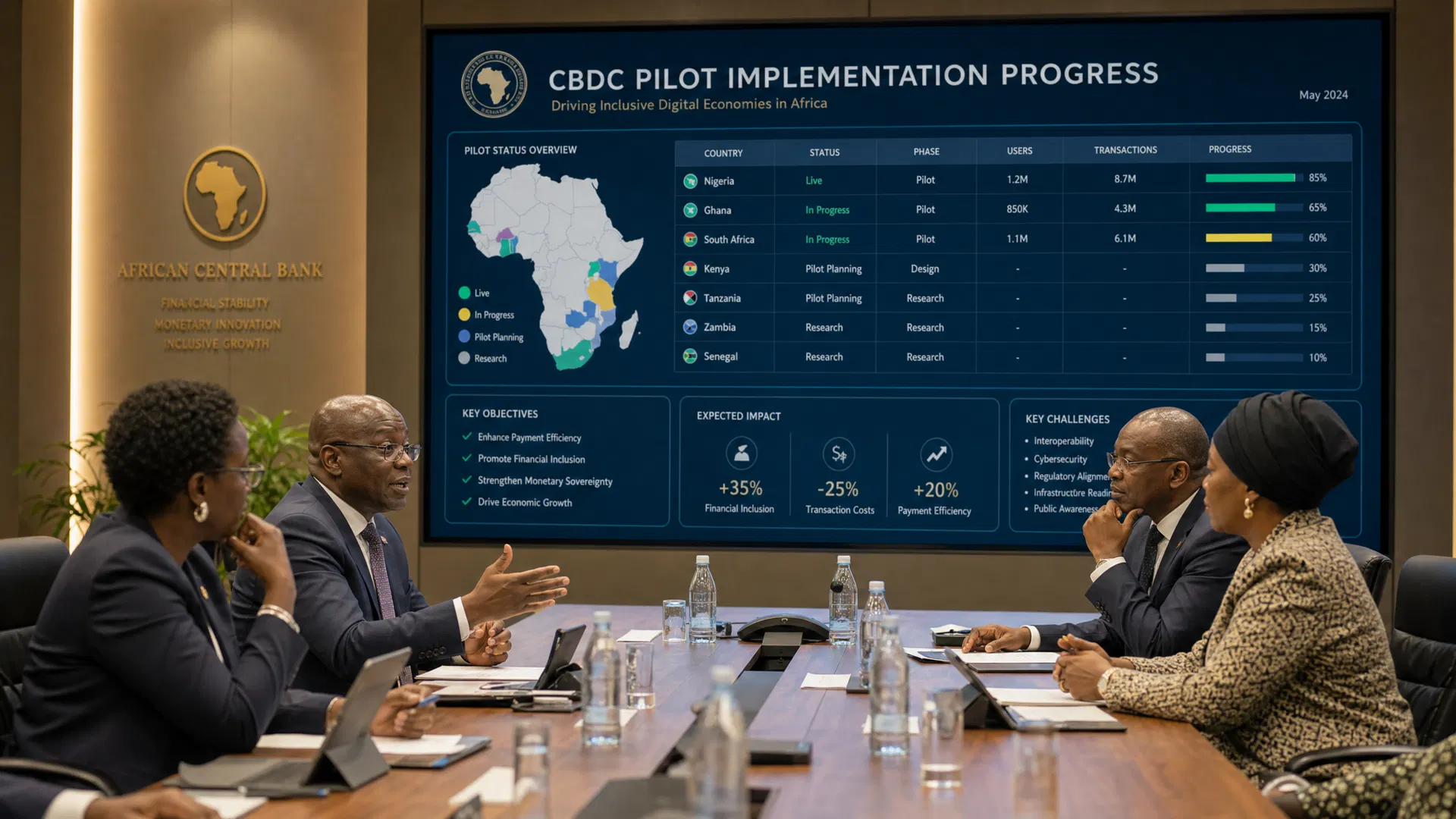

# Nigeria's Central Bank Digital Currency Regulations: The eNaira Regulatory Framework

The global financial ecosystem is undergoing a profound transformation, driven by the rapid digitization of assets and the emergence of sovereign digital currencies. At the forefront of this evolution in Africa is Nigeria, which made history on October 25, 2021, by launching the eNaira—the continent's first Central Bank Digital Currency (CBDC). For institutional investors, policymakers, and fintech operators navigating Africa's digital asset infrastructure, understanding the regulatory framework governing the eNaira is paramount. This framework not only sets the precedent for digital currency regulation in Nigeria but also serves as a critical reference point for regional harmonization efforts across the continent.

As AfriVest continues to build Africa's sovereign digital asset infrastructure—encompassing tokenization, CBDC integration, and digital identity—aligning with these regulatory standards is essential. The eNaira operates within a complex regulatory environment designed to balance innovation with financial stability, consumer protection, and anti-money laundering compliance. This article delves into the regulatory background, key provisions, compliance implications, and enforcement mechanisms of the eNaira, offering strategic insights for digital asset platforms operating in this dynamic landscape.

Regulatory Background and Legal Foundation

The regulatory foundation of the eNaira is anchored in the Central Bank of Nigeria (CBN) Act of 2007 and the Banks and Other Financial Institutions Act (BOFIA) of 2020. Pursuant to Section 19 of the CBN Act, the Central Bank of Nigeria issued the "Regulatory Guidelines on the eNaira," which took effect concurrently with the currency's launch in October 2021. These guidelines establish the eNaira as a direct liability of the CBN, equivalent in value to the physical Naira, and recognized as official legal tender.

The introduction of the eNaira was driven by several strategic objectives: deepening financial inclusion, facilitating more efficient and cost-effective cross-border remittances, reducing the informal economy, and enhancing the efficacy of monetary policy. Unlike decentralized cryptocurrencies, the eNaira is a centralized digital asset, administered through the CBN's Digital Currency Management System (DCMS). This centralized approach ensures that the CBN retains absolute control over the minting, issuance, distribution, and redemption of the digital currency, thereby mitigating the systemic risks often associated with unregulated digital assets.

Key Provisions of the eNaira Guidelines

The eNaira regulatory framework employs a two-tiered distribution model, clearly delineating the roles of the central bank and financial institutions (FIs). The CBN is exclusively responsible for the core administration of the eNaira, including its issuance and the management of the DCMS. Financial institutions, on the other hand, act as critical intermediaries. They are tasked with onboarding merchants and consumers, integrating eNaira wallets into their existing banking systems, and facilitating transactions.

A central component of the guidelines is the wallet architecture. The framework establishes distinct wallet types for different stakeholders: the eNaira stock wallet (held exclusively by the CBN), treasury wallets for financial institutions, and consumer/merchant wallets for end-users. To mitigate risks associated with capital flight and the disintermediation of commercial banks, the CBN implemented a Tiered Know Your Customer (T-KYC) structure. This structure imposes daily transaction limits (DTL) and eNaira wallet limits (EWL) based on the user's level of identity verification. For instance, Tier 0 users (unbanked individuals) face the most stringent limits, while Tier 3 users (fully verified individuals with Bank Verification Numbers) enjoy higher transaction capacities.

Compliance Implications for Digital Asset Platforms

For digital asset platforms and fintech operators like AfriVest, the eNaira framework introduces rigorous compliance requirements, particularly concerning Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT). The guidelines mandate that all financial institutions and participating platforms integrate robust AML/CFT checks within their eNaira operations. This includes continuous transaction monitoring, fraud detection, and strict adherence to the T-KYC protocols.

Furthermore, data protection is a critical compliance pillar. The operation of eNaira wallets involves the processing of sensitive personal and financial data, necessitating compliance with the Nigeria Data Protection Act (NDPA) of 2023. Platforms must ensure that their data handling practices align with the NDPA's principles of data minimization, purpose limitation, and secure processing. This domestic requirement also intersects with broader regional data protection standards, such as South Africa's POPIA, Kenya's DPA, and the Malabo Convention, which are crucial for platforms building pan-African infrastructure. Ensuring interoperability while maintaining stringent data privacy standards across these jurisdictions is a complex but necessary undertaking for institutional operators.

Enforcement Mechanisms and Risk Management

The CBN has established comprehensive enforcement mechanisms to ensure adherence to the eNaira guidelines. Financial institutions are required to implement sound enterprise risk management frameworks, encompassing robust IT security infrastructure, documented governance policies, and regular security assessments to mitigate cybersecurity threats. The CBN conducts periodic audits and requires regular reporting from FIs to monitor compliance and system integrity.

In the event of disputes or security breaches, the framework outlines specific resolution protocols. Financial institutions must provide dedicated channels for users to report lost or compromised wallets, and they are obligated to place prompt restrictions on affected accounts. Unresolved consumer complaints can be escalated to the CBN's eNaira Helpdesk, and ultimately, to an arbitration panel under the Arbitration and Conciliation Act. Failure to comply with the AML/CFT provisions, T-KYC limits, or reporting requirements can result in severe regulatory sanctions, including the suspension of eNaira operational privileges and substantial financial penalties under the BOFIA.

Preparing for Africa's Digital Economy Transformation

The eNaira represents a foundational step in Africa's broader transition toward a digitized, interconnected financial ecosystem. For digital asset platforms, preparing for this transformation requires a proactive and strategic approach to regulatory compliance. Platforms must invest in scalable, secure infrastructure that can seamlessly integrate with central bank systems like the DCMS, while simultaneously supporting international standards such as ISO 20022 for financial messaging.

As the regulatory landscape evolves, platforms must remain agile, anticipating future developments in CBDC interoperability and cross-border digital asset regulation. The eNaira framework provides a blueprint for how sovereign digital currencies can be integrated into the formal financial sector. By aligning with these regulations and prioritizing robust compliance, data protection, and risk management, platforms like AfriVest can position themselves as trusted partners in building the resilient, inclusive digital asset infrastructure that will drive Africa's economic future. The successful integration of CBDCs will not only enhance domestic financial systems but also pave the way for seamless, pan-African digital trade and investment.