The Rise of eNaira: Lessons Learned from Africa's First CBDC

Central Bank Digital Currencies (CBDCs) have emerged as a transformative force in global finance, offering new pathways for monetary policy, financial inclusion, and digital commerce. Africa, with its dynamic and rapidly evolving digital economy, has taken significant strides in this space. Notably, Nigeria launched the eNaira in October 2021, becoming the first African country to issue a CBDC. This pioneering initiative provides valuable lessons for policymakers, institutional investors, and stakeholders across the continent.

In this article, we explore the rise of the eNaira, examining its impact, challenges, and broader implications for Africa’s digital financial landscape.

---

Understanding the eNaira: Nigeria’s Digital Currency Ambition

The eNaira is a digital version of Nigeria’s fiat currency, issued and regulated by the Central Bank of Nigeria (CBN). It is designed to complement the physical Naira, making transactions faster, cheaper, and more accessible, particularly to the unbanked population.

As of mid-2023, Nigeria’s economy is the largest in Africa with a GDP exceeding $500 billion, and a population of over 220 million. Yet, less than 40% of adults have access to formal banking services, according to World Bank data. The eNaira aims to bridge this financial inclusion gap by leveraging mobile money and digital wallets, which already have significant penetration in Nigeria.

Key features of the eNaira include:

- Direct issuance by the Central Bank: Unlike cryptocurrencies, the eNaira is a sovereign liability, backed by the government.

- Interoperability with existing payment systems: It integrates with Nigeria’s existing banking infrastructure.

- Programmable and traceable transactions: This enhances transparency and reduces illicit financial flows.

- No interest-bearing: The eNaira functions as a digital cash substitute rather than a store of value.

---

Impact on Financial Inclusion and Payment Systems

One of the primary motivations behind the eNaira initiative is to enhance financial inclusion. Nigeria’s large informal economy and rural populations have historically faced barriers to accessing banking services. The eNaira, accessible via smartphones and feature phones, lowers these barriers by providing a low-cost digital payment alternative.

Since its launch, the eNaira has recorded over 2 million wallets created within its first year, according to the CBN. However, active usage remains a challenge, with transaction volumes still modest relative to the size of Nigeria’s payment ecosystem. For instance, mobile money transactions in Nigeria exceeded $30 billion monthly in 2022, dwarfing early eNaira activity, which signals room for growth.

The eNaira also supports faster cross-border remittances within the West African region. Remittances to Nigeria were estimated at $25 billion in 2022 by the World Bank, making it one of the top recipients globally. By reducing costs and settlement times, the eNaira could significantly improve the efficiency of these flows, benefiting households and SMEs.

---

Challenges and Lessons Learned

Nigeria’s eNaira rollout has not been without challenges, offering critical insights for other African nations contemplating CBDCs.

1. User Adoption and Public Awareness

Despite heavy publicity, many Nigerians remain unfamiliar with the eNaira’s features and benefits. Mistrust of digital financial products and concerns over data privacy have slowed adoption. This highlights the need for robust public education campaigns and transparent governance frameworks.

2. Interoperability and Infrastructure

The eNaira’s success depends on seamless integration with banks, mobile money operators, and merchants. Initial technical issues and bottlenecks underscored the importance of investing in resilient digital infrastructure and fostering collaboration between the central bank and private sector stakeholders.

3. Regulatory and Privacy Considerations

Balancing traceability for anti-money laundering (AML) purposes with user privacy rights remains a delicate task. Nigeria’s approach of programmable CBDC transactions offers a blueprint but requires ongoing policy refinement to ensure compliance with international standards while protecting citizen rights.

4. Monetary Policy Implications

The introduction of the eNaira has implications for liquidity management and monetary policy transmission. Central banks must carefully monitor CBDC’s impact on bank deposits and credit availability to avoid unintended financial instability.

---

Broader Implications for Africa’s Digital Economy

The eNaira represents a landmark step in Africa’s digital finance evolution, with several broader implications:

- Regional Integration: Nigeria’s leadership in CBDCs could catalyze a digital currency framework for the Economic Community of West African States (ECOWAS), facilitating seamless intra-regional trade and payments.

- Digital Identity and KYC: Coupling CBDCs with digital identity initiatives can strengthen Know Your Customer (KYC) processes, reducing fraud and enhancing access to formal finance.

- Innovation Ecosystem: The programmable nature of the eNaira opens opportunities for fintech innovation, including smart contracts and decentralized finance (DeFi) applications tailored for African markets.

- Financial Stability and Inclusion: Properly managed CBDCs can enhance financial resilience by providing a safer, more inclusive payment method during economic shocks.

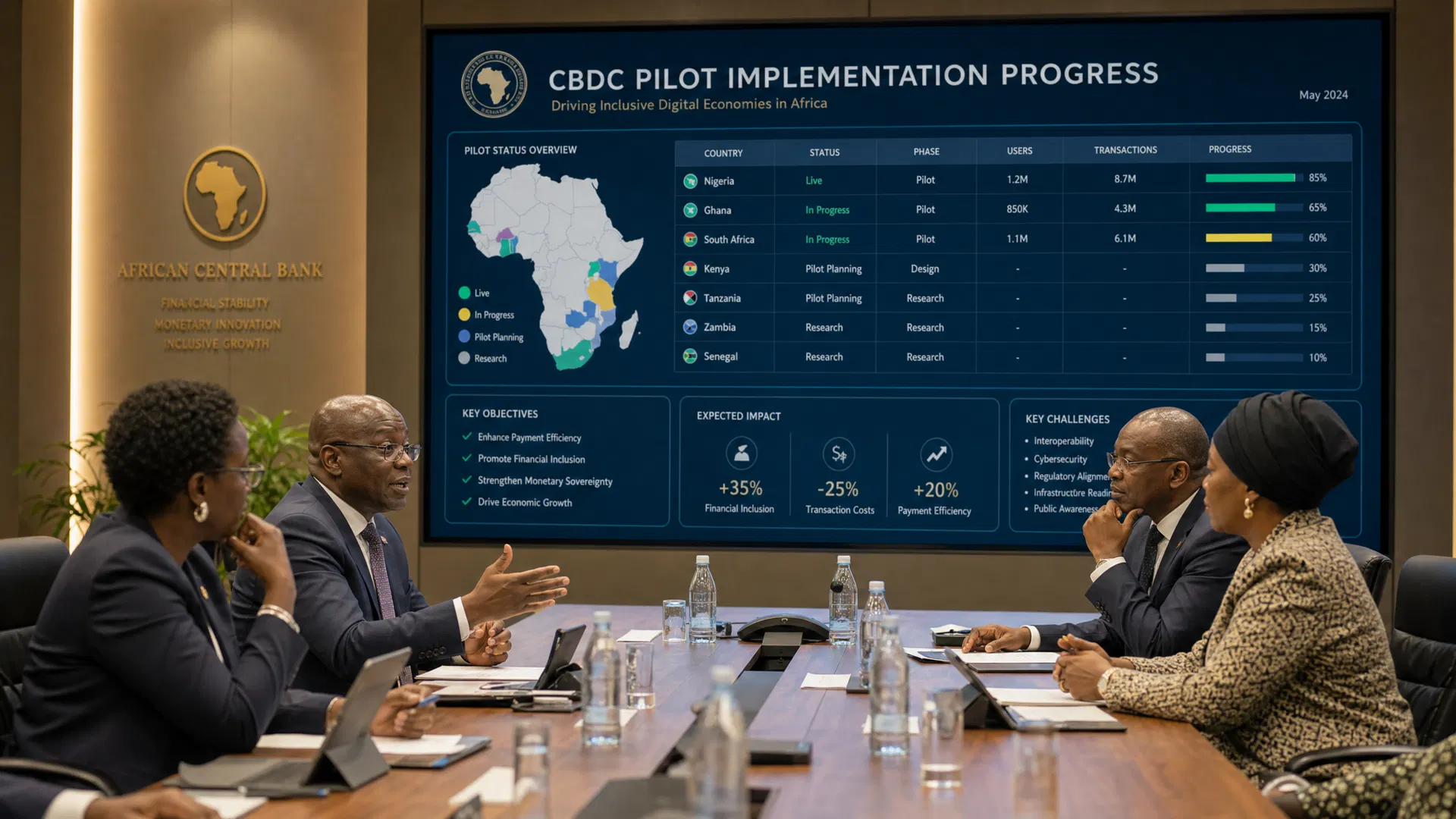

Other African countries are closely monitoring Nigeria’s experience. Ghana, South Africa, and the Central Bank of West African States (BCEAO) are actively developing their own CBDC pilots, informed by lessons from the eNaira’s implementation.

---

Conclusion

The rise of the eNaira marks a significant milestone in Africa’s journey toward a fully digital economy. While the journey has revealed challenges in user adoption, infrastructure, and regulatory balance, the initiative underscores the transformative potential of CBDCs in promoting financial inclusion, reducing transaction costs, and enhancing monetary policy effectiveness.

For institutional investors and policymakers, Nigeria’s eNaira experience offers a valuable case study in navigating the complexities of digital currency deployment in emerging markets. As Africa continues to embrace digital finance, the lessons from the eNaira will shape the future of monetary innovation across the continent.

---

References:

- Central Bank of Nigeria (CBN) eNaira Reports, 2023

- World Bank Global Findex Database, 2021

- World Bank Remittance Data, 2022

- African Development Bank, "Digital Financial Services in Africa," 2022