Securities Tokenization Regulations in African Capital Markets: Current State and Outlook

The African capital markets are undergoing a profound transformation, driven by the rapid adoption of digital assets and the tokenization of real-world assets. As institutional investors, policymakers, and fintech operators increasingly recognize the potential of distributed ledger technology to unlock liquidity and democratize access to capital, regulatory frameworks across the continent are evolving to keep pace. This shift is not merely technological but structural, requiring a delicate balance between fostering innovation and ensuring market integrity, investor protection, and financial stability. For platforms like AfriVest, which are building the sovereign digital asset infrastructure for Africa, navigating this complex regulatory landscape is paramount.

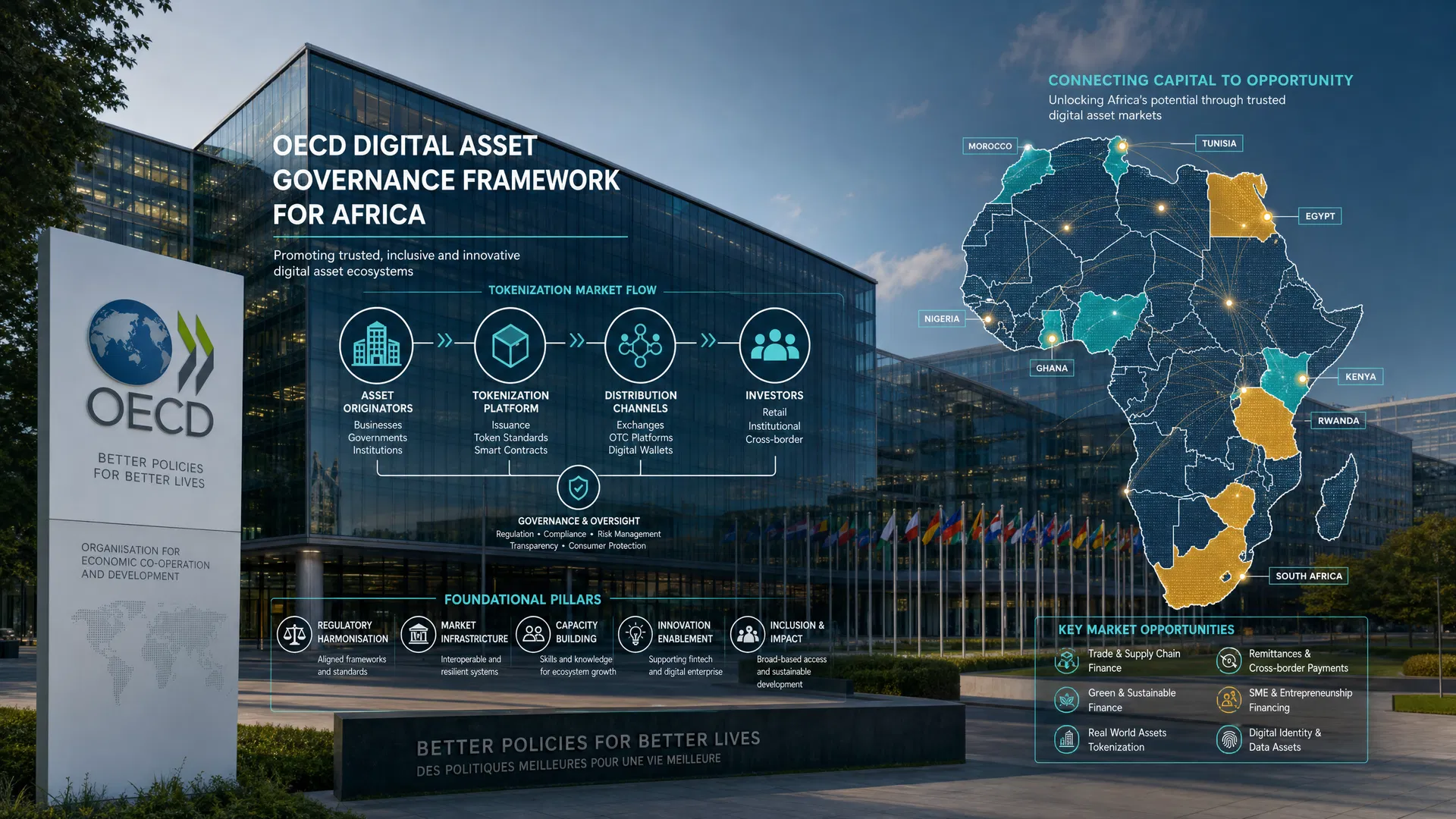

The regulatory background of securities tokenization in Africa is characterized by a transition from cautious observation to proactive engagement. Historically, African regulators approached digital assets with skepticism, often issuing warnings or outright bans due to concerns over money laundering, consumer protection, and capital flight. However, the narrative has shifted significantly. Recognizing the economic potential of tokenization—such as facilitating cross-border trade, enhancing financial inclusion, and mobilizing diaspora remittances—key jurisdictions are now establishing formal frameworks. This evolution is heavily influenced by international standards set by bodies like the Financial Action Task Force (FATF), the International Organization of Securities Commissions (IOSCO), and the Financial Stability Board (FSB). These global guidelines provide a foundational blueprint, encouraging African regulators to adopt risk-based approaches that classify tokenized assets based on their economic substance rather than their technological form.

Key provisions within emerging African regulatory frameworks focus on licensing, classification, and operational resilience. In South Africa, the Financial Sector Conduct Authority (FSCA) declared crypto assets as financial products in 2022, bringing them under the purview of the Financial Advisory and Intermediary Services (FAIS) Act. This requires Crypto Asset Service Providers (CASPs) to obtain licenses and adhere to stringent anti-money laundering (AML) and counter-terrorism financing (CFT) obligations. Similarly, Nigeria's Securities and Exchange Commission (SEC) issued rules on the issuance, offering platforms, and custody of digital assets in 2022, formally recognizing digital assets as securities. In Kenya, the Capital Markets Authority (CMA) has been actively exploring tokenization through its regulatory sandbox, while the recent Virtual Asset Service Providers (VASP) Act of 2025 establishes a dual-regulator model, dividing oversight between the Central Bank of Kenya and the CMA based on the nature of the asset. These frameworks consistently emphasize the need for robust governance, capital adequacy, and transparent disclosures.

The compliance implications for digital asset platforms operating in African capital markets are substantial. Platforms must implement comprehensive AML/CFT programs, including robust Know Your Customer (KYC) procedures and transaction monitoring systems, to comply with both local laws and FATF recommendations. Furthermore, data protection is a critical compliance pillar. Platforms must align their operations with regional data protection laws, such as South Africa's Protection of Personal Information Act (POPIA), the Nigeria Data Protection Act (NDPA), Kenya's Data Protection Act, and the broader Malabo Convention. This requires stringent data localization, consent management, and breach notification protocols. Additionally, platforms must ensure that their tokenization models comply with existing securities laws, particularly concerning prospectus requirements, secondary market trading, and settlement finality. The integration of ISO 20022 messaging standards is also becoming essential for ensuring interoperability with traditional financial systems and central bank digital currencies (CBDCs).

Enforcement mechanisms across the continent are becoming increasingly sophisticated. Regulators are moving beyond simple cease-and-desist orders to implementing comprehensive supervisory frameworks. This includes regular audits, mandatory reporting, and the deployment of on-chain analytics tools to monitor market activity in real-time. The Financial Intelligence Centres (FICs) in various jurisdictions are playing a central role in tracking illicit financial flows associated with digital assets. Penalties for non-compliance are severe, ranging from substantial financial fines to the revocation of licenses and criminal prosecution of platform operators. The collaborative approach among African regulators, facilitated by regional bodies and intergovernmental working groups, is also enhancing cross-border enforcement capabilities, making it increasingly difficult for non-compliant actors to engage in regulatory arbitrage.

To successfully navigate this environment, digital asset platforms must adopt a proactive and strategic approach to preparation. First, platforms should engage in continuous dialogue with regulators, participating in industry consultations and regulatory sandboxes to help shape future policies. Second, significant investment in compliance infrastructure is required. This includes deploying advanced regtech solutions for automated reporting, identity verification, and transaction surveillance. Third, platforms must prioritize legal structuring, ensuring that tokenized assets are accurately classified and that all necessary licenses are secured before launching products. Finally, building trust through transparency is crucial. Platforms should provide clear, accessible disclosures regarding the risks associated with tokenized securities, the underlying assets, and the technological infrastructure supporting the platform.

Looking forward, the tokenization of securities holds the potential to fundamentally reshape African capital markets. By reducing friction, lowering costs, and enabling fractional ownership, tokenization can unlock trillions in standby capital, driving investment into critical sectors such as infrastructure, agriculture, and small and medium-sized enterprises (SMEs). As regulatory clarity improves and institutional adoption accelerates, Africa is well-positioned to leapfrog traditional financial infrastructure and establish itself as a global leader in the digital economy. For platforms like AfriVest, the convergence of robust regulatory frameworks, advanced technology, and a deep understanding of the African market presents an unprecedented opportunity to build the foundation for a more inclusive, efficient, and resilient financial future. The journey from regulation to opportunity is underway, and the platforms that prioritize compliance and innovation will be the architects of Africa's digital asset transformation.