Rwanda's National Bank: CBDC Exploration and Digital Payment Regulatory Framework

The digital transformation of Africa's financial landscape is accelerating, and Rwanda is positioning itself at the forefront of this evolution. The National Bank of Rwanda (BNR) has embarked on a strategic exploration of a Central Bank Digital Currency (CBDC), alongside the introduction of a comprehensive regulatory framework for virtual assets. For institutional investors, policymakers, and fintech operators, understanding Rwanda's approach is crucial for navigating the future of digital finance in East Africa. This article delves into the regulatory background, key provisions, compliance implications, and enforcement mechanisms shaping Rwanda's digital asset ecosystem, offering insights for platforms like AfriVest as they build Africa's sovereign digital asset infrastructure.

Regulatory Background and the Push for Innovation

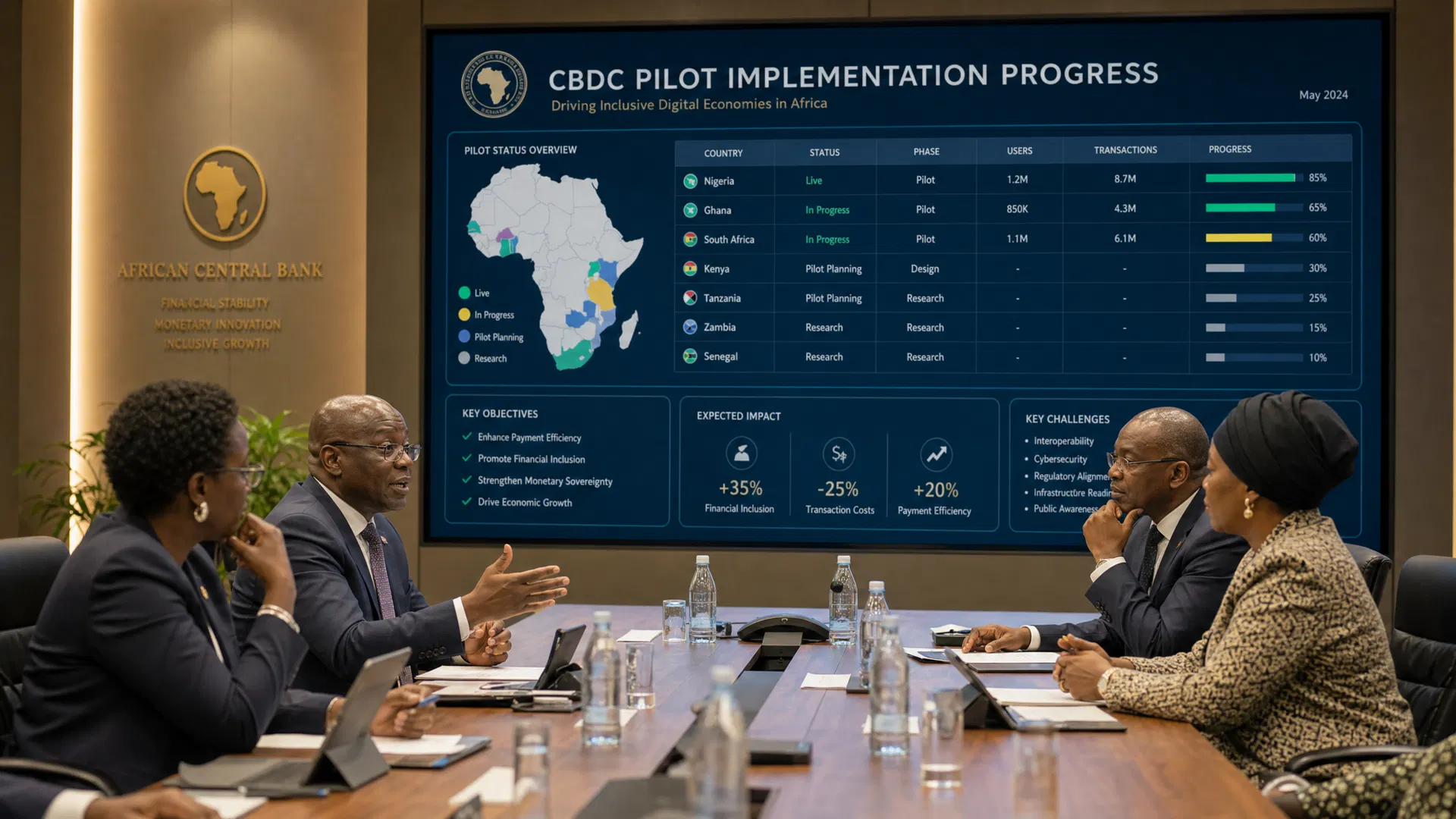

Rwanda's journey toward a digital economy is driven by a commitment to financial inclusion, innovation, and resilience. The BNR's exploration of a CBDC is motivated by four core objectives: strengthening payment resilience during network or power outages, promoting innovation and market competition, accelerating progress toward a cashless economy, and improving the efficiency of cross-border payments [1]. The central bank has initiated a five-month closed-loop proof-of-concept phase, expected to conclude in October 2025, involving staff from central and commercial banks, merchants testing offline payments, and institutions evaluating USSD features [1]. This phased approach underscores a disciplined strategy to understand user experience, technical feasibility, and potential risks, including cybersecurity and legal frameworks.

Concurrently, the Capital Market Authority (CMA) and the BNR have introduced a draft regulatory framework for virtual assets and Virtual Asset Service Providers (VASPs) [2]. Released for public consultation in March 2025, this framework aims to govern digital financial transactions, defining virtual assets as digital representations of value that can be traded, transferred, or used for payments and investments [2]. This definition encompasses assets represented on blockchain technologies, whether cryptographically secured or backed by collateral to maintain a stable value, reflecting a forward-looking stance on tokenization and digital representations of real-world assets.

Key Provisions of the Virtual Asset Framework

The proposed regulatory framework introduces several critical provisions designed to foster innovation while mitigating risks. A primary focus is addressing concerns raised by the Financial Action Task Force (FATF) regarding the potential misuse of virtual assets for money laundering and terrorist financing [2]. The regulations aim to provide clear guidance to the public and VASPs, ensuring secure, transparent, and regulated transactions.

One notable provision is the strict prohibition of using tokens to represent the Rwandan currency, a measure intended to prevent the misuse or manipulation of virtual assets [2]. Furthermore, the framework mandates that any legal entity wishing to conduct virtual asset services must apply for a license from the CMA, which will determine the specific requirements [2]. This licensing requirement is a pivotal step toward establishing a regulated environment where service providers are held accountable, and consumers are protected from fraudulent activities. The regulations also emphasize that sellers are legally obligated to deliver exactly what they have promised to buyers, addressing common issues in unregulated crypto trading where buyers often face significant losses [2].

Compliance Implications for Digital Asset Platforms

For digital asset platforms operating in or expanding to Rwanda, compliance with the new regulatory framework is paramount. Platforms must navigate the licensing requirements set forth by the CMA, ensuring that their operations align with the stipulated guidelines for VASPs. This includes implementing robust Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT) measures to satisfy FATF standards and local regulatory expectations.

Moreover, platforms must ensure compliance with regional data protection laws, such as Rwanda's Law relating to the protection of personal data and privacy (PDPA Rwanda), alongside broader frameworks like the Malabo Convention. As platforms like AfriVest build infrastructure covering tokenization, digital identity, and stablecoins, aligning with international standards such as ISO 20022, IOSCO, and IMF CBDC frameworks will be essential. The integration of CBDC into existing payment infrastructures will require platforms to adapt their technical architectures to support interoperability, secure offline payments, and efficient cross-border transactions, reflecting the BNR's core motivations for CBDC exploration.

Enforcement Mechanisms and Consumer Protection

The enforcement of the virtual asset regulatory framework will be overseen by the CMA, which will take on key responsibilities including ensuring compliance, licensing service providers, and overseeing virtual asset operations [2]. This regulatory oversight is designed to bring transparency to the market and protect consumers from the risks associated with unregulated trading.

In the interim, before the new regulations are fully approved and implemented, individuals affected by fraudulent virtual asset transactions can seek assistance from the Rwanda Investigation Bureau (RIB), which is responsible for handling financial crimes [2]. However, the current lack of a legal framework for crypto trading makes investigations complex and challenging for victims seeking justice. The formalization of the regulatory framework will provide clear rules, enabling open trading of virtual assets and empowering regulatory bodies to enforce compliance effectively, thereby enhancing consumer trust and market integrity.

Conclusion: Shaping Africa's Digital Economy Transformation

Rwanda's proactive approach to exploring a CBDC and regulating virtual assets marks a significant milestone in its digital finance journey. By establishing a clear legal framework and prioritizing financial inclusion, resilience, and innovation, Rwanda is positioning itself as a regional leader in inclusive and tech-driven financial systems. For platforms like AfriVest, Rwanda's regulatory landscape offers a blueprint for building sovereign digital asset infrastructure that aligns with international standards and regional data protection laws. As Africa's digital economy continues to transform, the integration of regulated virtual assets and CBDCs will play a pivotal role in driving economic growth, enhancing cross-border trade, and fostering a more inclusive financial ecosystem across the continent.

References

[1] TechAfrica News. (2025, August 1). National Bank of Rwanda Eyes Digital Currency Future with Targeted CBDC Testing. Retrieved from https://techafricanews.com/2025/08/01/national-bank-of-rwanda-eyes-digital-currency-future-with-targeted-cbdc-testing/

[2] Making Finance Work for Africa. (2025, March 9). Rwanda Moves to Regulate Virtual Assets With New Draft Law. Retrieved from https://www.mfw4a.org/news/rwanda-moves-regulate-virtual-assets-new-draft-law